For richer for poorer: has the Hogan Lovells union delivered on its promise?

While the 2010 merger of Hogan & Hartson and Lovells has gone more smoothly than many expected, on some counts it has underdelivered - can the firm kick on to the next level?

April 24, 2017 at 03:53 AM

18 minute read

The original version of this story was published on Law.com

In the small cadre of mega law firms that have used the Swiss verein corporate structure to span the globe, Hogan Lovells stands out. Call it the verein that doesn't look like a verein.

The verein structure is notable for the flexibility it gives international law firms, allowing them to combine cross-border without fully merging financial systems, including profit-sharing. In the seven years since US firm Hogan & Hartson joined forces with the UK's Lovells, the combined firm has taken a very different path from other verein firms such as Dentons and Norton Rose Fulbright, which were both formed at around the same time.

Where those firms have used their formative combinations as a platform for massive global expansion with a succession of bolt-on deals, Hogan Lovells has been steadily getting on with the job. Today Hogan Lovells is a solid, stable business that is integrated to the point of being virtually indistinguishable from any single-partnership firm, with roughly $1bn (£779m) of work referred between its two arms.

In fact, the combination is arguably the most successful transatlantic law firm merger of all time. "I don't think anyone has come close, honestly, to replicating what we did," former chair Warren Gorrell, now retired, says of the merger of equals he helped craft. The deal, completed in 2010, helped both firms resolve a troublesome international conundrum by providing each with the geographic component they lacked: Lovells with a strong US foothold; Hogan & Hartson with everything else.

Yet while the combination has gone more smoothly than even the firm expected, it has on some counts underperformed and underdelivered. Hogan Lovells' financial performance has lagged that of its key rivals and of the wider market, while to date the firm has been largely frustrated in its attempts to build a transactional practice that would allow it to win roles on the highest value deals. Should Hogan Lovells have aimed higher?

The combination was 10 times more difficult than I thought it would be. People just don't like change – particularly lawyers

At the time of the combination, both firms occupied clearly defined spaces in their respective markets. Lovells was one of the largest firms in London with a well regarded finance and disputes practice, but it was increasingly being squeezed out by larger, more profitable rivals, in the UK and globally. At the time of the merger, with 1,397 lawyers across 28 offices in 18 countries, the firm had gross revenue of $866m, revenue per lawyer (RPL) of $620,000 and profits per equity partner (PEP) of $1m.

Hogan & Hartson, meanwhile, was a top-tier firm in Washington DC, and a powerful player in the government regulatory and litigation spaces, but it lacked significant heft or brand recognition outside the US. It had 1,121 lawyers and in its last financial year before the combination, it reported revenue of $864.5m, RPL of $771,000 and PEP of $1.11m, with 27 offices across 11 countries.

Their complementary practice areas and similar financial profiles made the firms a good match on paper, but their leaders were determined to take every step to knit them together as seamlessly as possible.

When the two partnerships came to vote on the combination, in December 2009, the proposal presented to them was exhaustive in its detail – everything from the combined governance structure to a new compensation system and the allocation of assets and liabilities. Each practice group had a post-merger business plan, and both firms commissioned independent market reports on each other and on alternative merger candidates, which were distributed to partners. (The firm declines to name the alternative candidates.)

"One of the consequences of it being a genuine merger of equals was that we had honest conversations about the best way to do things, rather than just defaulting to the Hogan or Lovells way," deputy CEO David Hudd says. "That made a big difference."

For instance, Lovells had a strong tradition of holding contested elections for management positions, while Hogan & Hartson's senior management group was appointed by the executive committee. A compromise was reached: Hogan Lovells' board is elected, while other management positions are appointed.

Just as important was the personal side of integration. One London partner recalls that, directly before the vote, Hogan & Hartson management came to Lovells' 2009 partner conference in Lisbon, Portugal, to be quizzed by Lovells partners. "We were very paranoid about our culture, which we treasured," this legacy Lovells lawyer says. "We liked what we heard from them. A lot of US firms have mantras, and theirs was about being 'a great place to work', which they had written on the wall of their canteen in Washington."

Current CEO Steve Immelt (pictured) says that key to the firm's successful post-merger integration has been enabling partners from across the firm to regularly meet in person. The firm even developed bespoke software – 'Hogan Lovells Connect' – that enabled staff in different offices to communicate on a more personal and informal level. Local office champions were appointed to encourage employees of all levels to share information about their roles and outside interests.

Current CEO Steve Immelt (pictured) says that key to the firm's successful post-merger integration has been enabling partners from across the firm to regularly meet in person. The firm even developed bespoke software – 'Hogan Lovells Connect' – that enabled staff in different offices to communicate on a more personal and informal level. Local office champions were appointed to encourage employees of all levels to share information about their roles and outside interests.

"We invested a tremendous amount over a long period of time in getting people together, to build the relationships that allow a professional services firm to thrive," says Immelt. "If you really want to have a successful global strategy, it's not enough to have a map – you need a group of partners that are committed to working together and building client relationships."

Management also allowed practices and offices to retain some degree of operational flexibility. "Being integrated doesn't mean having the same approach to everything," says Immelt, adding: "You need to give people freedom and make sure they don't feel like they're being squashed by some overarching management bureaucracy."

One example is leverage. Generally speaking, the international arm is more highly leveraged than its US business. There are 2.9 lawyers for every equity partner in Hogan Lovells US, compared to 4.7 across its international network. "US partners have had to understand why a more highly leveraged practice might make sense – and why partners in that model don't bill 2,200 hours per year," Immelt says. Similarly, decisions regarding target billable hours for lawyers, support staff salaries and office space are all made locally.

The combined firm retained two co-chairs – Claudette Christian and John Young – until 2012, as well as joint practice heads, ensuring equal managerial representation from each legacy firm, but that dual approach was gradually phased out. Nicholas Cheffings was appointed global chair in 2012, while Immelt became sole global CEO in 2013. A year later, the firm's practices moved from having co-leaders to being led by a single global head each.

Excluding those who left the firm as a direct result of the combination, not a single one of the 26 partners interviewed for this feature had a negative word to say about the integration process. That's not to say the tie-up was easy, however. Some pruning was done: Hogan & Hartson's Warsaw and Hong Kong offices were cut, as was its Geneva office, while Lovells closed its branch in Chicago. Several sources say that "a handful" of partners from the legacy Hogan & Hartson London office left the firm.

"[The combination] was 10 times more difficult than I thought it was going to be," concedes Immelt. "People just don't like change – particularly lawyers – and that was true in every office around the world. There was a feeling that some people just wanted to dig in and make it difficult." He says he often used a phrase in management meetings at the time to describe the behaviour of certain partners: "Why make it easy when you can make it hard?"

Hogan Lovells decided to adopt the stricter US conflicts rules globally from day one, which Immelt says "took some getting used to". US conflicts rules are more restrictive than the UK system, particularly around taking an adverse position to clients. "It required a large number of people and a sophisticated IT system to deal with conflicts," says Asia-Pacific and Middle East managing partner Patrick Sherrington. "While there are probably more conflicts post-merger, that's an inevitable part of being a truly integrated global law firm."

The disparity between top earners on either side of the Atlantic was a point of contention. Some Hogan partners were paid as much as eight times more than any Lovells partner

Hogan Lovells says in a statement that "very few" conflicts arose as a result of the review and that it was able to negotiate waivers in "the vast majority" of these cases. The firm declined to comment on whether it lost clients post-combination over conflicts, but says: "The conflict rules tended more to impact the taking on of new clients and matters rather than existing ones."

Another big challenge was how to rationalise two disparate partner compensation systems. Like most top UK firms at the time, Lovells operated on a lockstep setup, with equity partners paid on the basis of seniority. Hogan & Hartson's compensation system, on the other hand, was built more around individual performance. As Immelt admits, the disparity between top earners on either side of the Atlantic was a point of contention. Some Hogan partners were paid as much as eight times more than any Lovells partner, according to sources with knowledge of the situation. "Did it create tension? Absolutely," Immelt says.

Hogan Lovells dropped the legacy Lovells lockstep altogether; now an equity point is worth the same, no matter where a partner is based. There are annual bonus pools for equity and non-equity partners, who are assessed on metrics such as billings, profitability, matter management, client-relationship management and origination as well as non-financial criteria.

"There was no doubt the amounts [paid to senior US partners] were considerably outside of the range of what we had as a lockstep," says a London partner, "but it opened your eyes to a brave new world of what you could earn in a meritocracy."

The firm says that the overall ratio in the firm between the top and lowest earners across the whole firm today is 10:1. While the gap between top earners in the US and UK remains – and the firm declined to give more details – one London partner says: "I think people are pretty mature about the remuneration structures. There obviously are people in the US who get paid a lot more, but the attitude of most is 'good luck to them'. These people bill millions. Some of the guys in the US bring in tens of millions of dollars."

Some felt the new compensation system did not go far enough. One former partner in London describes leaving the firm because of not "being properly rewarded". Immelt admits the firm's compensation system is "not perfect", but adds: "You have to strike a balance. You have to show that there is a path forward for top younger partners and that they won't be held back while senior partners are handsomely paid. But we're not an investment bank. We're not going to put everyone at zero each year and make them prove what they should be paid."

In addition to filling holes in respective geographic networks, the Hogan & Hartson-Lovells combination was also intended to provide a springboard to help move the new firm up the legal food chain, help it win more elite work for bigger multinational clients and ultimately become more profitable.

The disputes side has been a clear win, partners say. "We [Lovells] always considered ourselves at the very least one of the top two London firms for litigation," says Sherrington, former global head of litigation, "and Hogan & Hartson had a very significant litigation capability as well in New York and nationally in the US. Suddenly we had the ability to sell something much more credible to clients. Lovells had built a transatlantic capability for litigation, but it was relatively small compared to what you need to make a real impact in the US."

Another primary objective was to build top-end finance and corporate transactional practices, with a particular emphasis on London and New York. That effort has been less successful. When it comes to core transactional areas, Hogan Lovells' rankings in The Legal 500 directory have remained largely unchanged during the past six years. The firm's London office is still ranked no higher than the third tier for M&A, private equity, banking, acquisition finance, high yield and capital markets work. Its US arm, meanwhile, sits down in the fifth tier for M&A and private equity, and is not ranked at all for banking or global capital markets.

Data from Mergermarket shows that for M&A, the firm's sweetspot is not global megadeals, but transactions around $400m.

Certainly, Hogan Lovells has been involved in five of the 10 largest M&A deals in each of the past seven years, according to Mergermarket, including scoring a lead role advising Dell on its $24.4bn leveraged buyout in 2013. However, the firm appeared on the rest of the deals in more minor roles. When Dell bought IT storage provider EMC in 2015, for example, the company instead turned to Simpson Thacher & Bartlett to handle the $67bn deal, with Hogan Lovells supporting on matters including corporate, securities, foreign antitrust, and compliance and corporate governance.

Immelt is quick to highlight Hogan Lovells' work on Anheuser Busch InBev's record-breaking $106bn acquisition of UK brewer SABMiller as an example of the firm's improved standing within the M&A market. But the deal arguably proves the contrary. Despite a decade-long relationship with the firm – then general counsel John Davidson spent his entire career at legacy Lovells before joining SAB in 2006 – the company also brought in Linklaters for its expertise in big-ticket M&A, with Hogan Lovells taking a support role on corporate, securities, foreign antitrust, and compliance and corporate governance matters.

Last year, the firm advised clients that included GE Capital on the $1.4bn sale of its hotel loan portfolio and UK-based payment provider VocaLink Holdings on its $873m sale to MasterCard, and worked on the $2.8bn merger of US real estate company Parkway Properties with rival Cousins Properties.

"From a London perspective, we've made tremendous progress," says London corporate head Ben Higson. "Our corporate revenue has grown by more than 12% during the past three years, and we have had a number of really significant client wins." Global M&A head William Curtin concedes that the firm is still "climbing the mountain", but adds that it is currently looking at lateral partner recruitment opportunities in London and New York that could change its market standing.

In fairness to Hogan Lovells, neither of its legacy firms had particularly strong corporate practices, and there is arguably no harder feat in Big Law than attempting to break into the market for high-end M&A work in London and New York. Only a handful of firms, such as Gibson Dunn & Crutcher, Kirkland & Ellis and Latham & Watkins, have managed to do so.

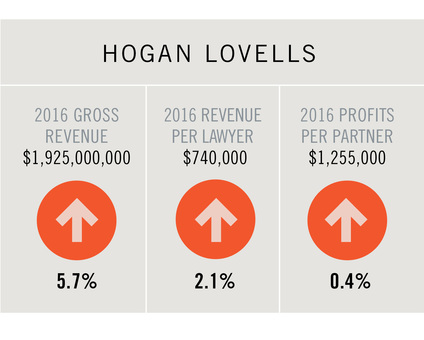

Harder to argue against is the fact that the firm has failed to make meaningful gains in its financial performance. Hogan Lovells' financials have lagged behind the Am Law 100 and Global 100 averages in both growth and absolute terms. In the six financial years after its combination, the firm's RPL has increased by 5% to $740,000, while PEP has grown 12.1% to $1.255m. The average Am Law 100 RPL, by comparison, has risen 13% during the same period, to $910,000, while the group's average PEP has leapt 21.6% to $1.66m.

Harder to argue against is the fact that the firm has failed to make meaningful gains in its financial performance. Hogan Lovells' financials have lagged behind the Am Law 100 and Global 100 averages in both growth and absolute terms. In the six financial years after its combination, the firm's RPL has increased by 5% to $740,000, while PEP has grown 12.1% to $1.255m. The average Am Law 100 RPL, by comparison, has risen 13% during the same period, to $910,000, while the group's average PEP has leapt 21.6% to $1.66m.

Immelt is quick to point out that due to the firm's global breadth, it is affected by currency fluctuations, such as recent declines in the value of the pound. "The clear impact of currency exchange rates can be seen when comparing performance measured in dollars versus sterling: If exchange rates had remained constant, we would have seen a revenue increase of 7.9%," Immelt says.

This doesn't change the fact that with financial performance lagging considerably behind its aspirational rivals, it has been hard for the firm to compete for big names. A current London partner concedes the firm can be too cautious about lateral hiring: "I think some slightly less conservative lateral hiring would be useful, and I would like to see some pretty big-name corporate and finance hires. I think that would propel us into the next level as you can only do so much with what you've got." In March, the firm made a big move in that direction, luring a four-partner Weil Gotshal & Manges Silicon Valley team led by technology transactions partner Richard Climan.

Despite the obvious challenges, Immelt says the firm's ultimate goal is to become an "exceptional global law firm that is competing for complex work at the highest end of the market", and cites both Latham and Skadden Arps Slate Meagher & Flom as its long-term competitors.

On the current evidence, that aim seems ambitious. Still, drawing on Hogan & Hartson's legacy in the US political capital, the firm boasts one of the strongest regulatory practices in the world. Hogan Lovells has deep sector strength in areas such as life sciences, in which it is ranked in tier two by the Legal 500, and its international network of 47 offices across 23 countries – plus associated offices in Budapest, Jakarta, Shanghai and Zagreb – is extensive and enviably balanced, with the US and the UK each accounting for around a third of the firm's total revenue.

Management's strategy also has the support of many within the firm. In interviews, numerous partners mention client opportunities that were unimaginable pre-combination. Co-head of the infrastructure, energy, resources and projects practice, Miguel Zaldivar, says the firm's work for the largest oil companies in Latin America – Petrogas, Petroleos Mexicanos, Petroleos de Venezuela and EP Petroecuador – would not have been possible pre-merger. He adds that as Chinese construction companies have moved into Latin America, "we've been able to successfully combine with the Beijing team to capitalise on this".

Even before the merger, Ford was a client of global finance head Sharon Lewis (pictured). Now it's one of several automakers that she represents. "I've got to know partners working with other automotive companies and I have a much better understanding of the automotive industry and its drivers," she says. "I've acted for BMW, VW, Peugeot and Fiat in ways that would not have been conceivable pre-combination."

Even before the merger, Ford was a client of global finance head Sharon Lewis (pictured). Now it's one of several automakers that she represents. "I've got to know partners working with other automotive companies and I have a much better understanding of the automotive industry and its drivers," she says. "I've acted for BMW, VW, Peugeot and Fiat in ways that would not have been conceivable pre-combination."

In an era where alternative merger structures are increasingly on the table, Hogan Lovells could serve as a case study of how to integrate two major Big Law practices, with the combined business almost certainly faring better than either of the legacy firms would have done alone. But also it represents something of a missed opportunity. Immediately after the combination, the firm was in the spotlight. It could perhaps have used that buzz and excitement to help attract a few marquee hires – the sort of star rainmakers who might have helped the firm get access to the premium work it craves.

That buzz has long since died. If the firm still harbours ambitions of rising to the top of the legal food chain, it will now have to claw itself up the hard way, along with everyone else. To do so will mean testing whether Hogan Lovells' risk-averse partnership will be culturally amenable to what will no doubt be a challenging – and costly – slog.

Overall, the union that created Hogan Lovells undoubtedly ranks as a very good merger. But with a bit more ambition and ruthlessness, it might have been great. As one former London partner puts it: "You could say that's why the combination has worked: because it hasn't been quite as aggressive as other firms. The downside, maybe, is that it hasn't been as aggressive as it could."

This content has been archived. It is available through our partners, LexisNexis® and Bloomberg Law.

To view this content, please continue to their sites.

Not a Lexis Subscriber?

Subscribe Now

Not a Bloomberg Law Subscriber?

Subscribe Now

NOT FOR REPRINT

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

You Might Like

View All

Legal Departments Gripe About Outside Counsel but Rarely Talk to Them

4 minute read

As Profits Rise, Law Firms Likely to Make More AI Investments in 2025

'Serious Disruptions'?: Federal Courts Brace for Government Shutdown Threat

3 minute read

'So Many Firms' Have Yet to Announce Associate Bonuses, Underlining Big Law's Uneven Approach

5 minute readTrending Stories

- 1Decision of the Day: Administrative Court Finds Prevailing Wage Law Applies to Workers Who Cleaned NYC Subways During Pandemic

- 2Trailblazing Broward Judge Retires; Legacy Includes Bush v. Gore

- 3Federal Judge Named in Lawsuit Over Underage Drinking Party at His California Home

- 4'Almost an Arms Race': California Law Firms Scooped Up Lateral Talent by the Handful in 2024

- 5Pittsburgh Judge Rules Loan Company's Online Arbitration Agreement Unenforceable

Who Got The Work

Michael G. Bongiorno, Andrew Scott Dulberg and Elizabeth E. Driscoll from Wilmer Cutler Pickering Hale and Dorr have stepped in to represent Symbotic Inc., an A.I.-enabled technology platform that focuses on increasing supply chain efficiency, and other defendants in a pending shareholder derivative lawsuit. The case, filed Oct. 2 in Massachusetts District Court by the Brown Law Firm on behalf of Stephen Austen, accuses certain officers and directors of misleading investors in regard to Symbotic's potential for margin growth by failing to disclose that the company was not equipped to timely deploy its systems or manage expenses through project delays. The case, assigned to U.S. District Judge Nathaniel M. Gorton, is 1:24-cv-12522, Austen v. Cohen et al.

Who Got The Work

Edmund Polubinski and Marie Killmond of Davis Polk & Wardwell have entered appearances for data platform software development company MongoDB and other defendants in a pending shareholder derivative lawsuit. The action, filed Oct. 7 in New York Southern District Court by the Brown Law Firm, accuses the company's directors and/or officers of falsely expressing confidence in the company’s restructuring of its sales incentive plan and downplaying the severity of decreases in its upfront commitments. The case is 1:24-cv-07594, Roy v. Ittycheria et al.

Who Got The Work

Amy O. Bruchs and Kurt F. Ellison of Michael Best & Friedrich have entered appearances for Epic Systems Corp. in a pending employment discrimination lawsuit. The suit was filed Sept. 7 in Wisconsin Western District Court by Levine Eisberner LLC and Siri & Glimstad on behalf of a project manager who claims that he was wrongfully terminated after applying for a religious exemption to the defendant's COVID-19 vaccine mandate. The case, assigned to U.S. Magistrate Judge Anita Marie Boor, is 3:24-cv-00630, Secker, Nathan v. Epic Systems Corporation.

Who Got The Work

David X. Sullivan, Thomas J. Finn and Gregory A. Hall from McCarter & English have entered appearances for Sunrun Installation Services in a pending civil rights lawsuit. The complaint was filed Sept. 4 in Connecticut District Court by attorney Robert M. Berke on behalf of former employee George Edward Steins, who was arrested and charged with employing an unregistered home improvement salesperson. The complaint alleges that had Sunrun informed the Connecticut Department of Consumer Protection that the plaintiff's employment had ended in 2017 and that he no longer held Sunrun's home improvement contractor license, he would not have been hit with charges, which were dismissed in May 2024. The case, assigned to U.S. District Judge Jeffrey A. Meyer, is 3:24-cv-01423, Steins v. Sunrun, Inc. et al.

Who Got The Work

Greenberg Traurig shareholder Joshua L. Raskin has entered an appearance for boohoo.com UK Ltd. in a pending patent infringement lawsuit. The suit, filed Sept. 3 in Texas Eastern District Court by Rozier Hardt McDonough on behalf of Alto Dynamics, asserts five patents related to an online shopping platform. The case, assigned to U.S. District Judge Rodney Gilstrap, is 2:24-cv-00719, Alto Dynamics, LLC v. boohoo.com UK Limited.

Featured Firms

Law Offices of Gary Martin Hays & Associates, P.C.

(470) 294-1674

Law Offices of Mark E. Salomone

(857) 444-6468

Smith & Hassler

(713) 739-1250