Are Wall Street law firms built to handle today's financial services industry?

Three emerging trends in the financial sector have created a new competitive landscape for traditional capital markets-oriented firms

August 21, 2018 at 12:00 AM

12 minute read

The original version of this story was published on The American Lawyer

Amid all the sound and fury about imminent disruption in legal markets, there is always one vaguely defined group assumed to be largely exempt from the coming maelstrom: the venerable and venerated white-shoe elites of Wall Street.

An air of permanence clings about these names, bolstered by the twin mystique of prestige and pedigree. It is perhaps fitting that Wall Street is named for the defensive wall that once guarded the shores of New Amsterdam before New York came to be. In much the same way, many of Wall Street's most elite law firms trace their roots back to a time that predates living memory. Their perennial prosperity, relatively undeterred by the shockwaves of the Great Recession, only reinforces the perception of unassailability.

In 2018, just how much of that perception is grounded in reality? How much of it is steeped in our cultural habit of unconscious mythmaking about the fabulously successful?

As financial markets undergo rapid technological changes and regulatory turmoil, the competitive landscape for high-end legal work in transactions and capital markets is also shifting. To examine whether the successes of Wall Street's storied past are likely to extend into an increasingly uncertain future, we revisit the key market conditions that fuelled the rise of Big Law's wealthiest incumbents and analyse three emerging megatrends in the financial sector.

The rise of the Wall Street elite: financial innovations demanded novel lawyering

The birth of the modern American financial markets can be traced as far back as the late 19th century, when monopolistic consolidation in railways, steel, oil and mining created unprecedented demand for capital investment. It is no accident that the oldest of the Wall Street law firms established themselves around the same time. To this day, many have maintained a stronghold on the most complex work in M&A transactions and capital markets. How? By being the first to fulfil a vital function in their clients' pursuit of a strategic leap forward.

In a seminal example, Sullivan & Cromwell first developed the concept of the holding company in the 1890s, allowing Edison General Electric and US Steel to sidestep existing antitrust law and integrate horizontally. The firm continued its rise to prominence by facilitating investment of European capital into American transcontinental railroads and the Panama Canal.

Over time, new models of corporate competition continued to emerge, directing M&A activity accordingly. As the financiers of Wall Street prospered, so did New York's most prestigious law firms. Throughout the 1970s and 80s, however, the fate of Wall Street took a singular turn as a few key developments conspired to create a decade of bonanza for New York's wealthiest bankers and lawyers.

In 1979, US monetary policy shifted toward a fixed money supply and floating interest rates. Interest-rate fluctuations led to greater price volatility in the secondary market for fixed-income products. Wall Street financiers went on to underwrite more debt and create new securities and derivatives to make secondary market trading more efficient. Many of these financial innovations in the bond market required new laws to be passed in Congress, existing laws to be reinterpreted and new debt instruments to be designed – all driving growing demand for specialised legal expertise.

Aggregate borrowing in the US underwent unbridled growth. In 1977, the combined debt of American governments, corporations and consumers totalled $323bn. Just eight years later, that figure was at $7trn. New bond issuances went through the roof, thanks to innovations in mortgage-backed securities led by Salomon Brothers and the explosion of high-yield junk bonds led by Michael Milken at Drexel Burnham.

Between 1977 and 1986, the mortgage bond holdings of US thrifts exploded from $13bn to $150bn. Cadwalader Wickersham & Taft and Cleary Gottlieb Steen & Hamilton essentially functioned as laboratories, churning out new securitisation methods for mortgage- and asset-backed securities as well as complex derivative products. Between 1984 and 1989, Cadwalader more than doubled its gross revenues while Cleary nearly tripled its top line.

Meanwhile, new junk bond issuance went from less than $900m in 1981 to $12bn in 1987. This turned out to be especially helpful to Wall Street law firms because Milken's junk bonds bankrolled the wave of hostile takeovers by corporate raiders throughout the 1980s, opening a floodgate of transactional work. Cahill Gordon & Reindel became the transactional adviser of choice for Drexel Burnham; by 1989, Cahill reported a profit margin of 59%, second only to Wachtell Lipton Rosen & Katz's staggering 71%.

The rise of the takeover and leveraged buyouts also created immensely lucrative second-order effects for law firms, driving M&A and securities litigation work. In addition, seemingly endless demand for new work sprang up to help raid-proof corporations by various legal means, like the famed poison pill defence developed by Marty Lipton at Wachtell. Also in the 1980s, legal work around companies' increased appetite for debt spiked, as did work on golden parachute contracts.

Wall Street law firms rode these waves in the financial markets to miraculous levels of growth and profit. With the exception of Cravath, all of the Wall Street firms nearly doubled in size from 1978 to 1988; the majority grew their top lines and net income by a multiple of between two and three. As a group, they would never again enjoy such an unblemished run.

Life beyond the 'Great Reset': three megatrends swirl around Wall Street

Wall Street 'capital markets' firms are often headquartered in a global financial centre, have deep relationships with a major bank, and have preferred access to the most intrinsically lucrative, high-margin practices.

In the 1970s and 80s, this description fit a sizeable group of New York firms. In 2018, the definition still fits, but less comfortably; the underlying competitive logic still holds sway, but the gloss of apex primacy is beginning to look a bit faded.

Our research and analysis identified three trends that conspire to erode the hegemony of the Wall Street law firm:

Structural changes to the banking industry stemming from consolidation. In the 1980s, a lengthy list of investment banks headquartered in New York controlled most M&A and capital markets activity on Wall Street. In 2018, most of those names have been washed away by multiple waves of consolidation. A few banks collapsed spectacularly, most notable of these being Drexel Burnham and Lehman Brothers, but most have been absorbed in some manner: Bear Stearns into JPMorgan Chase, Dean Witter into Morgan Stanley, First Boston into Credit Suisse, Salomon Brothers into Citigroup.

Only a handful of bulge brackets remain, operating globally as full-service investment banks, with a significant portion headquartered outside the US. In tandem with consolidation, banks have largely gone public; compared to the carefree excesses of the 1980s, investment banks are now subject to much more rigorous scrutiny by shareholders and regulators alike. The impact on law firms is nuanced but real. One result of consolidation is intensified pressure to manage costs across the enterprise; with growing size, banks are better positioned than ever to exploit economies of scale.

Case in point: earlier this year, JPMorgan Chase, Bank of America and Citigroup, which collectively arranged 20% of all bond issuances globally in 2017, agreed to jointly develop a new technology platform to streamline the disjointed bond issuance process for underwriters and asset managers. This proactive measure to displace the decades-old reliance on phone, email and the chat feature on the Bloomberg Terminal, is representative of a newfound focus on value and efficiency. This follows a 2015 announcement by Axiom Law of a multi-year $73m deal with a global bank to process master trade agreements and to streamline the back-office operations needed to maintain compliance.

In short, the established client base of the 'capital markets' law firm has shrunk in number and adopted buying preferences that are leaner and more value-conscious than ever before. The surviving banks now seek to make strategic investments into systemic solutions for proactive risk management and cost avoidance. Bulge brackets aren't likely to begin bargain shopping for high-consequence representation in the front office, but the newfound focus on value is real.

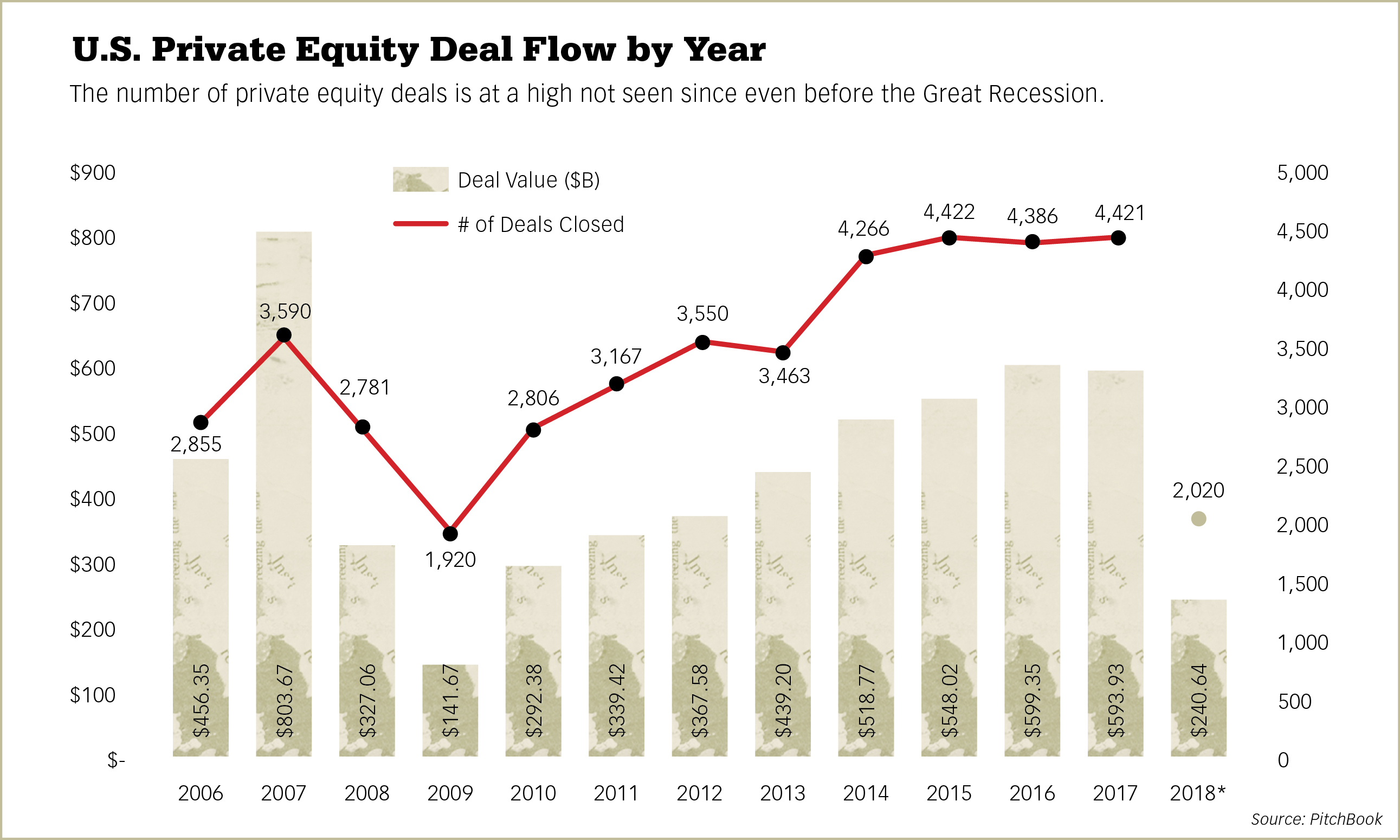

The rise of private equity and venture capital and the decline of public capital markets. The leveraged buyout of the 1980s served as a precursor to the rise of private equity in the 90s. Between 2000 and 2016, the number of private equity firms around the world tripled, while assets under management exploded from just under $600bn in 2000 to $2.8trn as of June 2017. Venture capital has also nearly doubled since the Great Recession, with $524bn in assets as of June 2017.

In contrast, the public markets show a decline: as a result of delisting, mergers and fewer initial public offerings, the number of publicly listed companies has fallen by more than half since 1996. This leaves law firms competing more intensely for fewer marquee clients in fewer megadeals, often engineered by players other than major investment banks.

While the old guard of New York still enjoy preferred access to marquee assignments to represent banks as underwriters, lenders or bookrunners, they lack the same type of preferred access to the new class of investors and financiers poised to dominate the most vital sectors and regions of the global economy.

The scope of capital market flows now extends far beyond New York's borders. Old-line Wall Street firms now face fierce competition on all sides and from outside their ranks: from ascendant global powerhouses like Kirkland & Ellis and Latham & Watkins, both aggressively targeting private equity; Silicon Valley strongholds with closer ties to VCs and the high-tech sector, like Wilson Sonsini Goodrich & Rosati, Cooley, and Fenwick & West; and an emergent class of more competitively priced globals vying for share in Asia.

Regulatory upheaval and innovation in the financial sector. Regulatory burden is a favoured complaint of big business across all sectors. The conservative thinktank Competitive Enterprise Institute reports that the US Government issued more than 80,000 pages of rules in 2015 and estimates the total cost of compliance at $1.9trn. There is no question that the post-crisis financial reforms have dampened Wall Street's profits. JPMorgan Chase has hired more than 8,000 compliance professionals since the 2008 crisis, and Deloitte estimates that the operating costs spent on compliance by financial service institutions increased by 60% between 2008 and 2016.

Under the Trump Administration, deregulation is de rigueur once again, creating opportunity for both banks and law firms alike. However, cyclical changes in regulatory regime represent only one lever in the growing complexity around financial services. Even if Dodd-Frank reforms were repealed entirely or rolled back significantly, banks are unlikely to wholly dismantle their compliance infrastructures, which consist not only of people but also process-driven systems as well as proprietary data, knowledge networks and accumulated investments in regtech and fintech.

A more likely scenario is a value-oriented bifurcation of regulatory work: high-stakes assignments to leading firms for premium rates and the continuing build-out of internal capabilities to operationalise day-to-day compliance and to service high-volume enforcement and litigation needs.

In 2018, financial innovation tends to apply emerging technology to new mechanics and channels to move capital through the financial system. Algorithmic trading, 'dark pools' and cryptocurrency are all examples of new frontiers where regulators and legislators lag in articulating safeguards around a rapidly changing financial sector. While their broad impacts on the economy are uncertain, such innovations are likely to provide a steady flow of grist for new controls and ongoing showdowns with regulators – and more canny lawyering by expert specialists.

Wachtell, Sullivan & Cromwell, Paul Weiss Rifkind Wharton & Garrison, Debevoise & Plimpton, Davis Polk & Wardwell and Cleary are all well positioned to compete for lucrative work in the regulatory space. However, competition for high-consequence, high-profile assignments will be fierce, varied and blindingly pedigreed from every direction. Depending on the specific opportunity, K Street stalwarts, litigation specialists, Kirkland, Skadden Arps Slate Meagher & Flom and Latham are all likely to put themselves in play.

Position isn't destiny, but still an advantage

These megatrends knit together to create a new competitive landscape for the old-line capital markets firms – but new doesn't mean bad. Analysis of backward-looking data shows most of the old-line elite are still fabulously prosperous.

But the slowdown of revenue-per-lawyer growth in the post-recession recovery and the rising intensity of competition suggest that in the future, the old guard of New York will experience at least relative levels of winning and losing.

In 2018, the old-line Wall Street firms still enjoy significant advantages to compete and win. What has changed since their heyday is that they must now actually compete, in arenas far-flung from New York and as diverse as Silicon Valley, Washington DC and China. For all firms except Wachtell – sui generis in more ways than one – perpetual dominance across key metrics is no longer guaranteed simply by virtue of the poshest address in Big Law.

Jae Um is the founder of Six Parsecs and an ALM Intelligence fellow. Nicholas Bruch is a senior analyst with ALM Intelligence.

NOT FOR REPRINT

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

You Might Like

View All

Trending Stories

- 1Tesla, Musk Appeal Chancery Compensation Case to Delaware Supreme Court

- 2Some New Twists and Old Tricks for an Ethical New Year

- 3TikTok Hit With California Class Action for Allegedly Mining Children's Data Without Parental Consent

- 4New York Latest to Adopt NextGen Bar Exam

- 5People in the News—Jan. 9, 2025—Rawle & Henderson, Armstrong Teasdale

Who Got The Work

Michael G. Bongiorno, Andrew Scott Dulberg and Elizabeth E. Driscoll from Wilmer Cutler Pickering Hale and Dorr have stepped in to represent Symbotic Inc., an A.I.-enabled technology platform that focuses on increasing supply chain efficiency, and other defendants in a pending shareholder derivative lawsuit. The case, filed Oct. 2 in Massachusetts District Court by the Brown Law Firm on behalf of Stephen Austen, accuses certain officers and directors of misleading investors in regard to Symbotic's potential for margin growth by failing to disclose that the company was not equipped to timely deploy its systems or manage expenses through project delays. The case, assigned to U.S. District Judge Nathaniel M. Gorton, is 1:24-cv-12522, Austen v. Cohen et al.

Who Got The Work

Edmund Polubinski and Marie Killmond of Davis Polk & Wardwell have entered appearances for data platform software development company MongoDB and other defendants in a pending shareholder derivative lawsuit. The action, filed Oct. 7 in New York Southern District Court by the Brown Law Firm, accuses the company's directors and/or officers of falsely expressing confidence in the company’s restructuring of its sales incentive plan and downplaying the severity of decreases in its upfront commitments. The case is 1:24-cv-07594, Roy v. Ittycheria et al.

Who Got The Work

Amy O. Bruchs and Kurt F. Ellison of Michael Best & Friedrich have entered appearances for Epic Systems Corp. in a pending employment discrimination lawsuit. The suit was filed Sept. 7 in Wisconsin Western District Court by Levine Eisberner LLC and Siri & Glimstad on behalf of a project manager who claims that he was wrongfully terminated after applying for a religious exemption to the defendant's COVID-19 vaccine mandate. The case, assigned to U.S. Magistrate Judge Anita Marie Boor, is 3:24-cv-00630, Secker, Nathan v. Epic Systems Corporation.

Who Got The Work

David X. Sullivan, Thomas J. Finn and Gregory A. Hall from McCarter & English have entered appearances for Sunrun Installation Services in a pending civil rights lawsuit. The complaint was filed Sept. 4 in Connecticut District Court by attorney Robert M. Berke on behalf of former employee George Edward Steins, who was arrested and charged with employing an unregistered home improvement salesperson. The complaint alleges that had Sunrun informed the Connecticut Department of Consumer Protection that the plaintiff's employment had ended in 2017 and that he no longer held Sunrun's home improvement contractor license, he would not have been hit with charges, which were dismissed in May 2024. The case, assigned to U.S. District Judge Jeffrey A. Meyer, is 3:24-cv-01423, Steins v. Sunrun, Inc. et al.

Who Got The Work

Greenberg Traurig shareholder Joshua L. Raskin has entered an appearance for boohoo.com UK Ltd. in a pending patent infringement lawsuit. The suit, filed Sept. 3 in Texas Eastern District Court by Rozier Hardt McDonough on behalf of Alto Dynamics, asserts five patents related to an online shopping platform. The case, assigned to U.S. District Judge Rodney Gilstrap, is 2:24-cv-00719, Alto Dynamics, LLC v. boohoo.com UK Limited.

Featured Firms

Law Offices of Gary Martin Hays & Associates, P.C.

(470) 294-1674

Law Offices of Mark E. Salomone

(857) 444-6468

Smith & Hassler

(713) 739-1250