Litigation Funders Face Their Hardest Sell: Big Law

There is more money than ever in the hands of litigation financiers. But can they convince law firms to use it?

June 28, 2018 at 12:47 PM

18 minute read

Credit: Richard Mia.

Credit: Richard Mia.

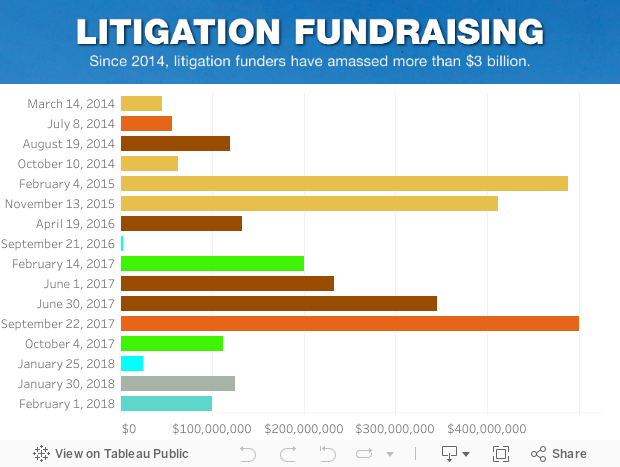

When the two largest rivals in an industry combine, it is typically a sign of a mature market. In the case of litigation finance, throw that rule out. The December 2016 acquisition of Gerchen Keller Capital by Burford Capital—at the time the two largest companies investing in commercial litigation—has proved to be a spark plug for the nascent business of financially backing lawsuits.

Before it was acquired, Chicago-based Gerchen Keller boasted to be the world's largest litigation financier, having raised $1.3 billion. In the 18 months since its sale, major funders in the U.S. have announced raising $1.75 billion to put toward new cases. That is more than three times the amount raised in the 18 months prior to Burford's acquisition. Eight different funds or debt issuances have raised more than $100 million since GKC's sale; there were just three capital raises of that size in the prior three years.

Longford Capital exemplifies the growth of investors' appetites in litigation finance in the U.S. Started by two former partners of a Chicago-based, 100-lawyer firm, Neal Gerber & Eisenberg, Longford launched a fund with $56.5 million in 2014. In September 2017, it coaxed nearly nine times that amount from investors, announcing that its second fund had closed at $500 million. The firm now estimates there is up to $5 billion in capital committed to commercial litigation finance in the U.S. and up to 30 money managers operating in the space.

Make no mistake: There has never been more capital looking to finance corporate litigation, and it is only expected to grow. There are at least two funds poised to launch by the end of the year. And to hear their pitches, funders are eyeing the nation's largest law firms as potential borrowers.

But there is still a long way to go before litigation funders can say they're closing deals with a majority of the Am Law 200 or even financing a significant portion of their litigation. In order to achieve that level of market penetration, industry insiders say funders must clear two major hurdles: Lower the price of their capital and make it easier to close deals in a timely and consistent manner.

“The combination of the high cost of capital and the often slow and clunky process for actually getting a deal done is already and will continue to restrict possible growth in this space,” says James Blick, head of U.S. operations at litigation finance broker The Judge. “The market will have to change in order to grow beyond a certain point.”

On that longer-term point, most everyone agrees. As capital continues to increase in the industry, financing in the legal business will mature the way other financial markets have. Financiers will find more ways to spend the money they've raised; the money will get cheaper; returns for funders will fall; and maybe, along the way, the management of litigation risk will fundamentally change.

The other challenges that funders face are on the demand side. While funders are faulted for having too many hoops to jump through, Big Law firms are often heaving bureaucracies themselves. Even if a commercial litigator is on the verge of a deal with a funder, he or she may have to run it up the rungs of the firm leadership. And, while awareness of funding is growing, funders were starting from a low base.

Lucian Pera, an attorney with Adams and Reese who counsels the litigation funding brokerage Westfleet Advisors on ethics issues, says his own firm's leadership is “sensitizing themselves to the availability” of litigation finance. “But I don't think we've done a single deal like that,” he adds.

The Cost of Capital

Litigation finance in the United States is little more than a decade old, but the market for litigation lending has already undergone some significant change.

Burford's first investments, for instance, came in 2009. Its performance from cases in that first year are representative of the possible outcomes for litigation funders and how much they've grown in the years since.

Three of Burford's 2009 cases are completed, according to its financial records, which do not provide details of the underlying cases. The first case was an investment of $7 million—its largest investment that year that has concluded. That case brought the type of astounding returns that attract investors. Burford recovered $38.1 million, returning a profit more than four times its investment. A second investment of $2 million broke even for Burford, carrying a $2 million recovery. A third, of $2.5 million, was a total loss.

Last year, Burford's average investment size was $24 million, up from $3 million just five years ago. Yet the business has the same all-or-nothing risk as always. Funders call this a “binary risk,” and it makes litigation funding more expensive than other types of finance. Funders often ask for returns on their capital ranging from three to six times the amount they invested; a percentage of a final fee award; or some combination of that structure.

Referring to his prior job, Burford CEO Christopher Bogart says, “As GC of Time Warner, I don't know if I would have done a single-case [funding] deal because the cost of capital is pretty expensive.”

In an effort to reduce that cost, Burford and others have sought to finance a number of cases at a time for a given law firm or legal department. So-called “portfolio financing” greatly reduces the odds of a total loss—even if one case goes belly up, it's unlikely five will—and, in turn, funders demand a smaller return on their money.

There are a handful of publicly known portfolio deals. Burford says it invested $100 million in a global firm's commercial litigation cases; $50 million in another large firm's arbitration cases; and $45 million to fund cases for a company that was later reported to be British Telecommunications. Last year alone, Burford says it committed $726 million to portfolio deals, compared with $72 million in single-case deals.

With the rules of supply and demand, you might think that all the money pouring into litigation finance would make capital cheaper. So far, that hasn't been the case. Funders and others close to the industry say that's because demand for their money—particularly from the Am Law 200—has grown along with their cash. There's also a limit to how low funders can go, because of what they tell investors about expected returns.

“We believe in our space there is a 1 percent market penetration for commercial litigation finance,” says William Farrell Jr., a co-founder of Longford Capital. “As capital has increased in our asset class, the demand for our financing has increased at an even faster rate.”

While few expect the industry will grow to 100 times its current size, the returns that funders have generated so far for investors suggest they do not lack for winning cases. But litigation finance hasn't yet accomplished what many believe it can: reshaping the billing models and risk appetites of Big Law firms' litigation practices and corporate America's legal departments.

Aiming at Am Law

There is pressure on litigation funders to get money out the door. They have been increasingly seeking to cut large deals with the Am Law 200, not just the boutiques and other small-to-midsize firms that were among the earliest adopters of litigation finance. According to funders and some litigators, financiers are making inroads.

In March, Burford said it was funding cases handled by 40 different firms. Its largest relationship with a law firm (described as a “global, enormous firm” by chief investment officer Jonathan Molot) comprised 14 percent of the 877 ongoing matters it was financing.

“The difference between five years ago and now is marked,” says Allison Chock, chief investment officer at Bentham IMF, one of the largest litigation funders in the U.S.

Chock, a former litigator at Latham & Watkins and McKool Smith, says when she joined the Australia-headquartered outfit in 2013, Bentham was not as enthusiastic about marketing to larger firms stateside.

“Large firms have a lot of red tape, and so it was harder to get the deal through,” Chock recalls. A big part of what has changed, she surmises, is the sustained financial pressure on Big Law firms and the hourly billing model. “It seems like it's only a matter of time before that collapses,” she says.

You might think litigation funding would slow the death of the hourly billing structure by shifting the burden of paying lawyers' hourly fees from clients to funders. Not necessarily. Chock says Bentham—like most funders—typically pushes for the firm to accept at least a partial contingency deal.

“We do have a handful of full hourly deals, but it's not our preferred way of doing things, because we like an alignment of interests between us, the lawyers and the claimant,” she says.

As a result of those financial pressures, law firms are starting to centralize how they manage and price legal work, says Lee Drucker, co-founder of litigation funder Lake Whillans. Pooling information about cases within a firm makes it easier for funders to talk with law firm managers about which cases are a good fit for funding, Drucker adds.

Another way to explain the greater adoption of litigation funding by Big Law is that it's client-driven, says Jay Greenberg, CEO of Boston-based LexShares. His company is chiefly an online platform that lists cases for qualified investors. But this year it also took a more active role in the market with the launch of a $25 million managed fund that invests in a portion of the full slate of cases listed on LexShares.

“I don't think clients want to engage with counsel on litigation on a pure hourly basis,” Greenberg says. The other factor driving greater adoption, he says, is the heightened profile of the industry. “I think that clients are becoming more aware, law firms are becoming more aware, and law firms are getting more comfortable.”

In January, at ALM Media's Legalweek conference, Gary Miller, co-chair of Shook, Hardy & Bacon's business litigation practice, said on a panel that his firm had used litigation finance. He said clients are increasingly seeking alternative fee arrangements, but there are relatively few cases his firm would take on a straight contingency basis.

Growing Pains

Though adoption of litigation funding may seem to be growing anecdotally, numbers are hard to obtain. Funders jealously guard information about deal flow, and getting a concrete sense of which firms have the best cases for investment is not straightforward. Because of that, it's also not easy to say whether successfully courting Big Law is an imperative for the litigation financiers from a pure business perspective.

“It's a very difficult market to quantify,” Greenberg says. “We know it's a large market, but it's an opaque market.”

While most players in the industry believe there is ample and growing demand for today's current funders, the level of interest among law firms is still difficult to gauge.

“We don't need to live in a world where Skadden is financing $500 million in cases tomorrow for today's funders to be successful,” says an industry executive who requested anonymity to speak freely. “Those [big firms] are coming around. It's pretty slow, but they're coming around. But is there room for 10 more Burfords? No. Not at the current size.”

Even if demand isn't keeping funders up at night, some say other concerns are hindering the growth of litigation finance, including the high cost of their funds for law firms. Some of the world's largest firms already are more prone to fund their own contingency fee cases, unwilling to split their profits. Those portfolios can be lucrative for large firms and are the most profitable practices at some, says David Desser, founder of Chicago-based litigation funder Juris Capital.

“If law firms are smart with growing their alternative-rate business, their realization rate will be higher for that portfolio of matters than it will be for any other group of matters,” Desser says. “Everyone who shares some of that data with me shows me very plainly that is the most profitable practice in their firm.”

The cheaper capital that comes with folding cases into a portfolio hasn't convinced everyone that it is a worthwhile deal. Craig Martin, head of the litigation department at Jenner & Block, says he believes law firms will grow more comfortable committing a larger portion of their fees to contingent cases. That will not necessarily require taking out funding agreements for those portfolios.

“Thus far, I haven't seen the appeal of those,” Martin says. “But large litigation departments would be interested in them, including us.”

Kirkland & Ellis has been comfortable taking on the risks of contingent fees without a corresponding increase in its use of litigation funding. Partner Reed Oslan has run his firm's contingent fee practice since about 2000. While he says the firm's clients often have interest in litigation finance, Kirkland traditionally funds its own special fee cases. Oslan declined to comment on why, but one reason may be that the firm's partnership can afford the risk thanks to its $4.7 million in profits per partner.

So, why hasn't the price gone down? Burford's Bogart says there are two main reasons: the high level of risk in the market and investors' high expected returns.

“The fact of the matter is people lose litigation cases,” Bogart says. “And the impact of those losses is very significant. That is the most significant impact on capital pricing. Because you need to price to overcome the losses.”

Bogart says Burford's returns have been analogous to a “well-performing” private equity business, which is a level of returns that he says needs to continue “to be attractive to investors.”

Another constraining factor is the amount of work and time required to close deals. Nick Rowles-Davies, formerly of Burford and Vannin Capital, launched a fund last year, Chancery Capital, with $100 million in funding. At the time, he said he wanted to make capital easier to access for corporate clients. “The existing market is too expensive, too rigid, too template-driven, and is way too competitive,” Rowles-Davies told CDR Magazine.

Is Big Law the Right fit?

Another limiting factor in litigation finance's rise is that it doesn't necessarily fit with some significant Big Law practice areas. Funders are typically looking for commercial plaintiff-side contingency suits as investment vehicles. But that's hardly the majority of what Big Law firms do. They do deal work, defense-side work in labor and employment and product liability cases, and a slate of plaintiff-side cases where hourly fees are still fully covered. Even if some Am Law 100 firms make half their revenue from litigation, only some fraction of that work is suitable for funding.

Consider Winston & Strawn as an example. The Chicago-founded firm's chairman, Tom Fitzgerald, says the firm invests 1 to 2 percent of its work in progress in contingent-fee cases. But the firm doesn't use funding on all those cases. Notably, the firm self-financed its contingent-fee representation of a beef manufacturer in a libel case against Walt Disney Corp. that last year led to a settlement of at least $177 million (details of the settlement remain confidential). Fitzgerald says the firm never considered third-party financing for that case. It reserves it for what he calls “generational cases.”

“They'll require investment over a long period of time and then have an event that creates liquidity far in the future,” Fitzgerald says. “In that type of situation, the partners that make the investment don't always get the return. And so, in that situation, we do think about funding to address that generational issue.”

Broadening firm leaders' thinking about what cases make sense to fund is a main objective for many funders. But for now, litigation finance is often used in a handful of practice groups and when plaintiffs with good cases are otherwise in dire financial straits. A good chunk of what large firms do is transactional work that doesn't readily lend itself to litigation finance. Funders are trying to edge into that space, too, by offering to finance or otherwise monetize an acquisition target's “litigation assets,” or legal claims the company may be able to bring, making it a more attractive deal.

“Certain practice areas lend themselves more readily to litigation finance—such as IP and bankruptcy. And it's lawyers within these practice areas who are encouraging their firms to explore litigation finance,” says Andrew Langhoff, who did business development at Burford and Gerchen Keller before starting brokerage Red Bridges Advisors. International arbitration, he says, “is an area especially well-suited for litigation finance.”

“These cases are typically very expensive to bring, take many years to resolve, and often involve very large awards,” Langhoff adds. “Using other people's money just makes sense.”

King & Spalding is one of the few firms that has publicly used litigation finance in such a case—an investor-state arbitration against Argentina. Burford financed that case and sold its interest in the award earlier this year, making $94.2 million. It was one of the earliest transactions in what may be an emerging secondary market for litigation finance deals.

An Evolving Future

Whatever the medium-term challenges may be for litigation funders, many are convinced that financing is here to stay.

The price of litigation funding could come down if there were better ways to gauge and measure litigation risk. That is one idea behind a litigation finance startup called Legalist, which says it offers “data-backed litigation financing.” Legalist says its algorithms trawl “tens of millions” of court records to “accurately and efficiently” assess litigation risk.

Many people think that sort of litigation prediction is a long way away. One partner at a global firm says today's biggest funders are not using large data sets to analyze litigation risk. The partner, who declined to be identified discussing relationships with funders, says funders have referred to that idea as “the genius business.”

“They say we don't actually quantify the litigation. We don't have to be geniuses. We can just try to figure out whether the case has a likelihood of some amount of damages awarded,” he says. “That's why they believe it's easier to do. And they've got a point.”

Prices could drop if investors with different risk appetites enter the space. Some in the industry predict insurance companies or investment banks may enter the market with large pools of capital ready to be deployed for smaller returns.

“Most of the entities in this space are special-purpose funds where capital has been raised from investors specifically for the purpose of investing in litigation and they are looking for very high-risk, high-return opportunities,” says The Judge's Blick. “But as soon as institutional capital starts to flood into this space, things will change. And that is a risk issue.”

Some speculate there may be a way to create tradeable securities based off of litigation risk. The idea of “securitization” of litigation funding assets could create a more robust market for risk that could lower prices. Longford's Bill Strong, a former top executive at Morgan Stanley, suggested at a presentation in New York City in May that such a market could develop. Bogart is less optimistic.

“You need an awful lot of capital to achieve real portfolio diversification that is actuarially meaningful,” he says.

Oslan, the Kirkland & Ellis partner, says he sees relatively few funders making large returns because of a general lack of competition in a sizable market.

“As it matures, develops and becomes more commoditized, cheaper capital will flow into the market and it should behave in exactly the same way other capital markets and financial instruments have over the years,” Oslan says. “The question is whether we're currently in the second inning, third inning or sixth inning. And, of course, whether it's a nine-inning game.”

Email: [email protected] or [email protected]

Correction: Bentham secured a total of $112 million (AUD$150 million) in fundraising in October 2017. It did not raise additional funds that month. We regret the error.

This content has been archived. It is available through our partners, LexisNexis® and Bloomberg Law.

To view this content, please continue to their sites.

Not a Lexis Subscriber?

Subscribe Now

Not a Bloomberg Law Subscriber?

Subscribe Now

NOT FOR REPRINT

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

You Might Like

View All

Adding 'Credibility' to the Pitch: The Cross-Selling Work After Mergers, Office Openings

5 minute read

Law Firms Are 'Struggling' With Partner Pay Segmentation, as Top Rainmakers Bring In More Revenue

5 minute read

Will a Market Dominated by Small- to Mid-Cap Deals Give Rise to a Dark Horse US Firm in China?

Trending Stories

- 1Ephemeral Messaging Going Into 2025:The Messages May Vanish But Not The Preservation Obligations

- 2Decision of the Day: Trial Court's Sidestep of 'Batson' Deprived Defendant of Challenge to Jury Discrimination

- 3Is Your Law Firm Growing Fast Enough? Scale, Consolidation and Competition

- 4Child Custody: The Dangers of 'Rules of Thumb'

- 5The Spectacle of Rudy Giuliani Returns to the SDNY

Who Got The Work

J. Brugh Lower of Gibbons has entered an appearance for industrial equipment supplier Devco Corporation in a pending trademark infringement lawsuit. The suit, accusing the defendant of selling knock-off Graco products, was filed Dec. 18 in New Jersey District Court by Rivkin Radler on behalf of Graco Inc. and Graco Minnesota. The case, assigned to U.S. District Judge Zahid N. Quraishi, is 3:24-cv-11294, Graco Inc. et al v. Devco Corporation.

Who Got The Work

Rebecca Maller-Stein and Kent A. Yalowitz of Arnold & Porter Kaye Scholer have entered their appearances for Hanaco Venture Capital and its executives, Lior Prosor and David Frankel, in a pending securities lawsuit. The action, filed on Dec. 24 in New York Southern District Court by Zell, Aron & Co. on behalf of Goldeneye Advisors, accuses the defendants of negligently and fraudulently managing the plaintiff's $1 million investment. The case, assigned to U.S. District Judge Vernon S. Broderick, is 1:24-cv-09918, Goldeneye Advisors, LLC v. Hanaco Venture Capital, Ltd. et al.

Who Got The Work

Attorneys from A&O Shearman has stepped in as defense counsel for Toronto-Dominion Bank and other defendants in a pending securities class action. The suit, filed Dec. 11 in New York Southern District Court by Bleichmar Fonti & Auld, accuses the defendants of concealing the bank's 'pervasive' deficiencies in regards to its compliance with the Bank Secrecy Act and the quality of its anti-money laundering controls. The case, assigned to U.S. District Judge Arun Subramanian, is 1:24-cv-09445, Gonzalez v. The Toronto-Dominion Bank et al.

Who Got The Work

Crown Castle International, a Pennsylvania company providing shared communications infrastructure, has turned to Luke D. Wolf of Gordon Rees Scully Mansukhani to fend off a pending breach-of-contract lawsuit. The court action, filed Nov. 25 in Michigan Eastern District Court by Hooper Hathaway PC on behalf of The Town Residences LLC, accuses Crown Castle of failing to transfer approximately $30,000 in utility payments from T-Mobile in breach of a roof-top lease and assignment agreement. The case, assigned to U.S. District Judge Susan K. Declercq, is 2:24-cv-13131, The Town Residences LLC v. T-Mobile US, Inc. et al.

Who Got The Work

Wilfred P. Coronato and Daniel M. Schwartz of McCarter & English have stepped in as defense counsel to Electrolux Home Products Inc. in a pending product liability lawsuit. The court action, filed Nov. 26 in New York Eastern District Court by Poulos Lopiccolo PC and Nagel Rice LLP on behalf of David Stern, alleges that the defendant's refrigerators’ drawers and shelving repeatedly break and fall apart within months after purchase. The case, assigned to U.S. District Judge Joan M. Azrack, is 2:24-cv-08204, Stern v. Electrolux Home Products, Inc.

Featured Firms

Law Offices of Gary Martin Hays & Associates, P.C.

(470) 294-1674

Law Offices of Mark E. Salomone

(857) 444-6468

Smith & Hassler

(713) 739-1250