A Crack in the Wall: Elite Wall Street Firms Are Being Put to the Test

The once-impenetrable facade of some of the country's sturdiest law firms is showing signs of wear in the face of shifting financial markets. Now they are forced to confront a once-foreign concept: competition.

August 19, 2018 at 06:00 AM

26 minute read

Credit: Taylor Callery

Credit: Taylor Callery

James Clark's phone rang at 4 a.m. with a message that would have been unthinkable to the Wall Street deal lawyer just months earlier.

The bleary-eyed Cahill Gordon & Reindel partner heard the terms of a deal he had helped to negotiate: a plan to stave off insolvency for residential mortgage giant GMAC. Cahill had handled the initial financing on behalf of client Bank of America. “This is the final deal, and we hope you like it,” Clark says he was told that morning in December 2008, “because President Bush is going live with it in three hours.”

To follow a conversation on this subject between ALM Intelligence senior analyst Nicholas Bruch and The American Lawyer editor-in-chief Gina Passarella beginning Aug. 28, register here:

With the financial crisis deepening, the moment underlined a dramatic shift in power away from the financial services industry. It was just one of many firsts for Wall Street lawyers and their firms over the past decade, as a core client base—investment banks—lost some of its influence.

Read these related pieces:

Are Wall Street Firms Built to Handle Today's Financial Services Industry?

Why we Looked at Wall Street Firms

Podcast: Are Wall Street Firms Losing the Talent War?

Since the collapse of Lehman Brothers a decade ago, the New York legal market has seen seismic shifts, from the boom and bust of financial services litigation, to banks placing ever more severe fee pressures on firms, to bank regulation helping tilt the playing field toward a booming private equity industry. At the same time, a growing midmarket deal base has opened the door for other firms to enter the M&A arena. Alternative service providers count Wall Street banks as major clients, and general counsel are paring back their stable of outside firms. Banks are also handling more of their own matters, as much of the work becomes more “plain vanilla,” Morgan Stanley's Eric Grossman told The American Lawyer last fall. “My firm, we have a dozen firms that are doing litigation/regulatory/internal investigation work,” Grossman said. “I'm not going to be able to feed a dozen firms going forward.”

For law firms—especially the elite Wall Street club—that means pressure to adapt or risk lower profits.

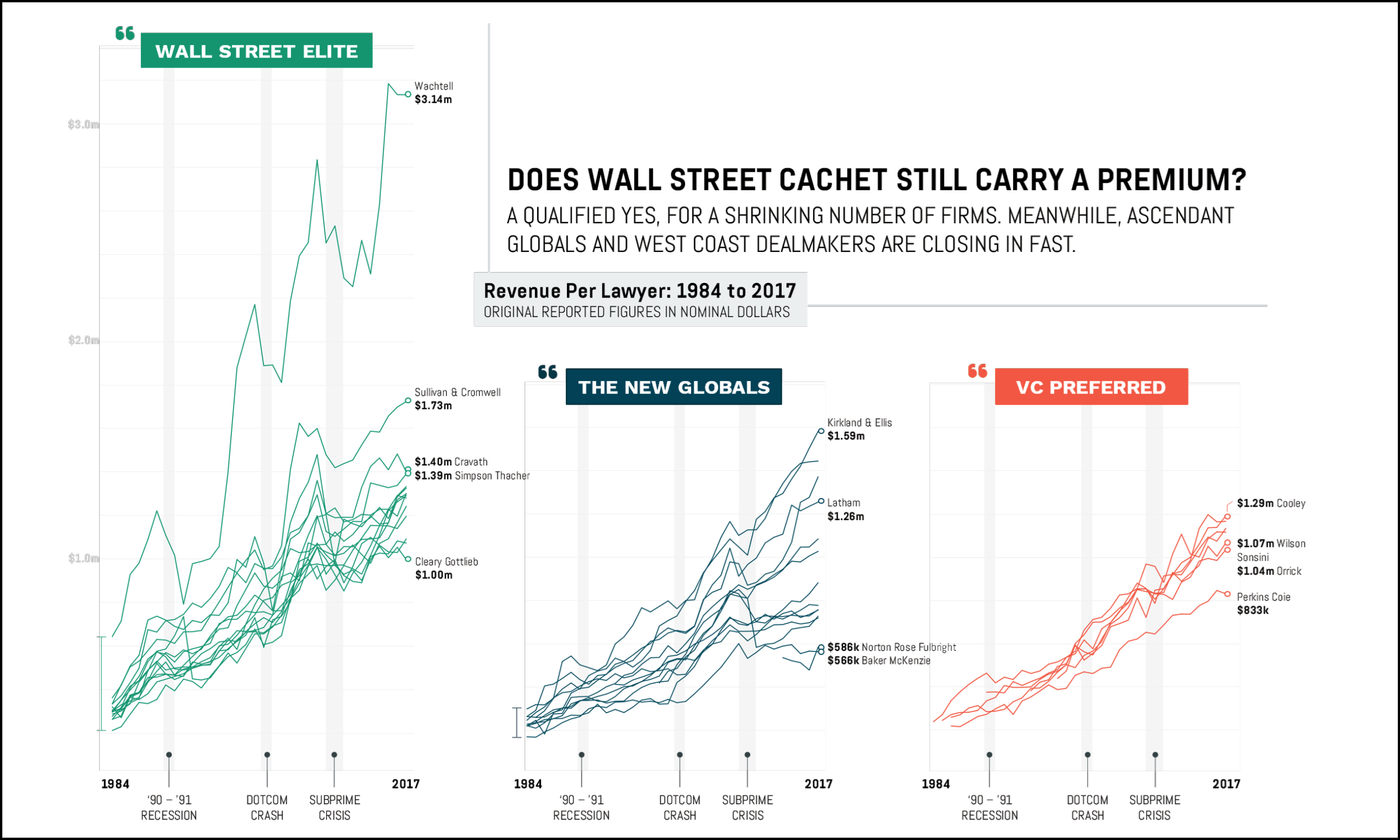

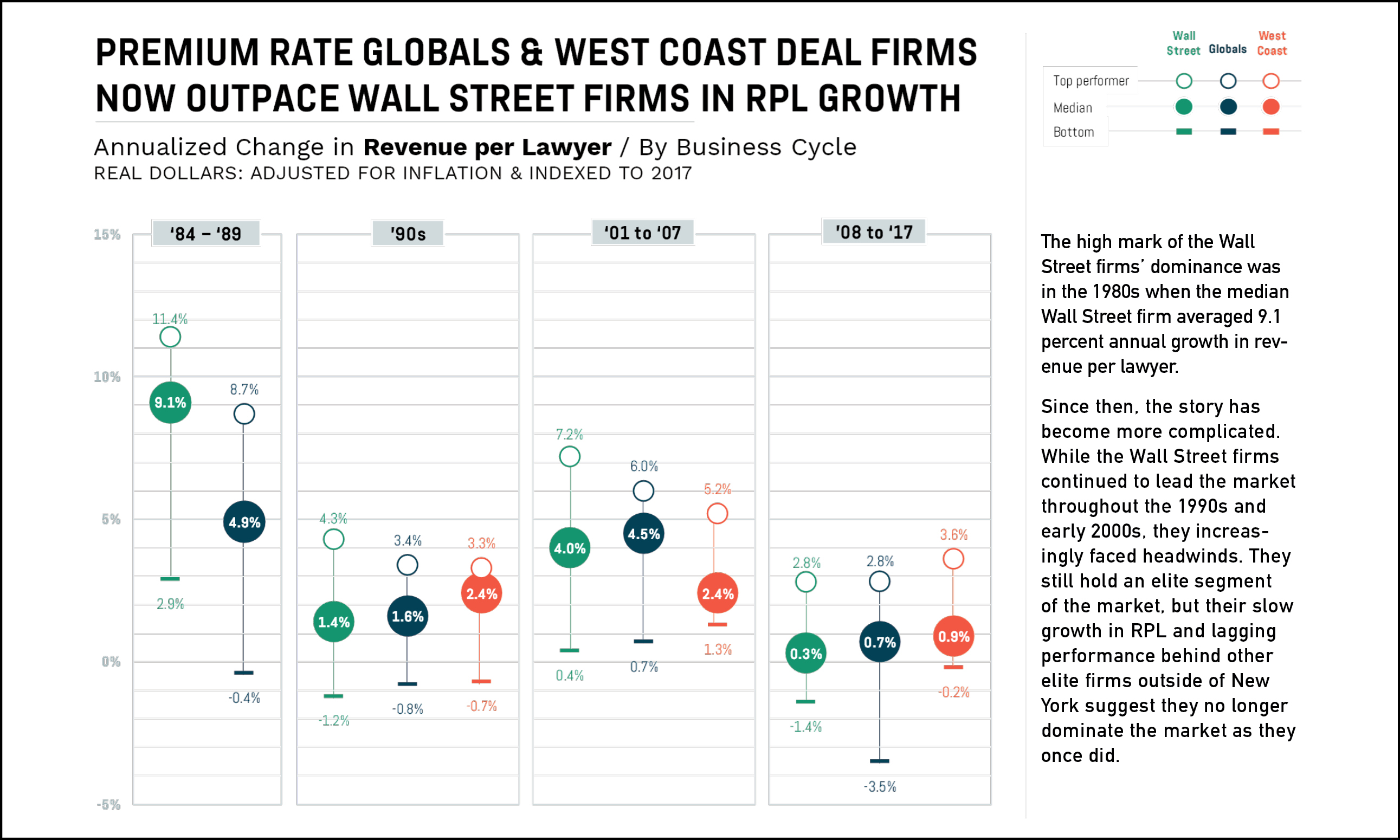

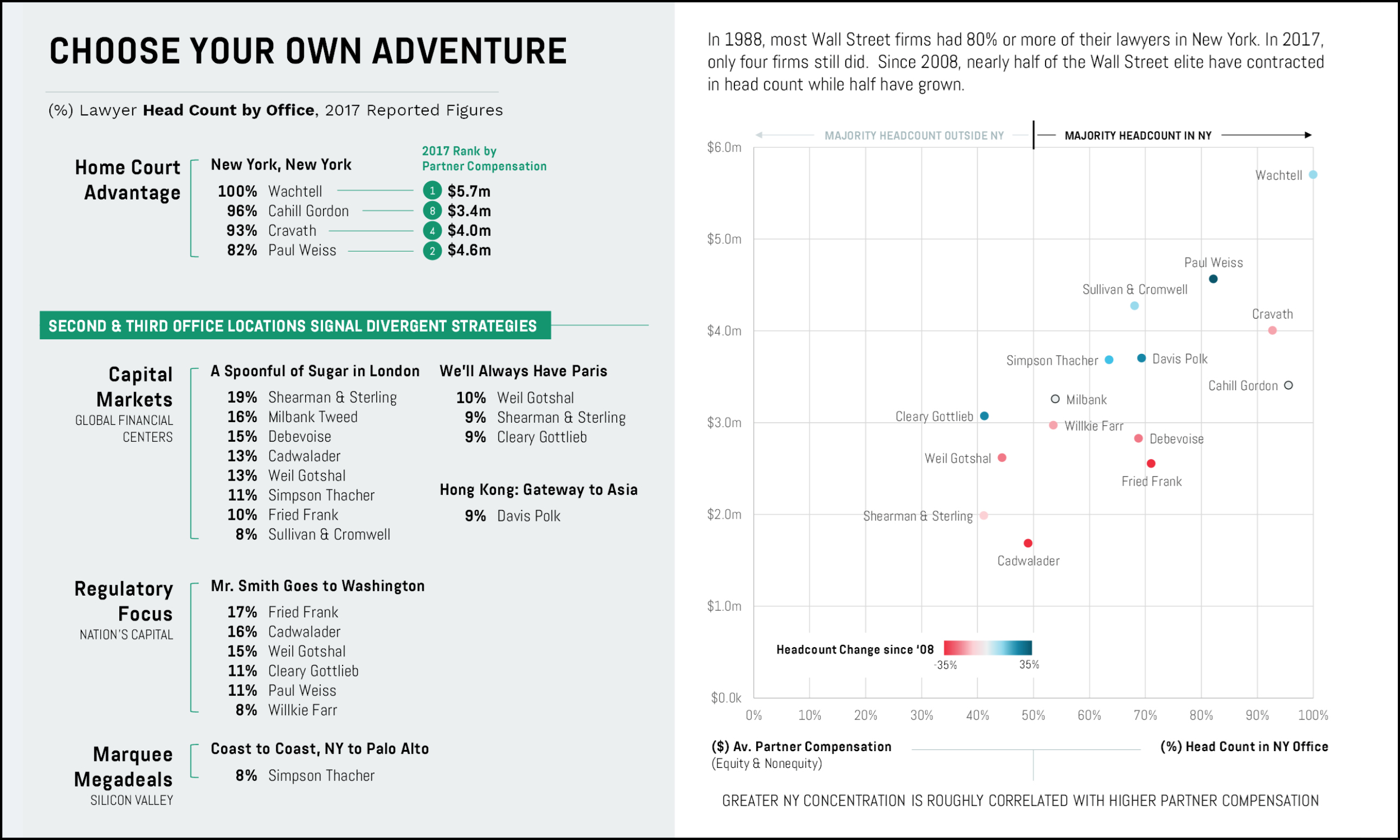

It's not a large club—15 firms. But as a group, it accounts for 15.6 percent of the Am Law 100's total revenue and, historically, attracts the very top talent out of law school and government. It's also a group that is bullish, at least publicly. Wall Street law firm leaders say deal work is booming, and most can boast strong revenue and profits to show for it.

The 15 firms included in our look at Wall Street were: Cadwalader, Wickersham & Taft; Cahill Gordon & Reindel; Cleary Gottlieb Steen & Hamilton; Cravath, Swaine & Moore; Davis Polk & Wardwell; Debevoise & Plimpton; Fried, Frank, Harris, Shriver & Jacobson; Milbank, Tweed, Hadley & McCloy; Paul, Weiss, Rifkind, Wharton & Garrison; Shearman & Sterling; Simpson Thacher & Bartlett; Sullivan & Cromwell; Wachtell, Lipton, Rosen & Katz; Weil Gotshal & Manges; Willkie Farr & Gallagher.

But with a decline in financial services litigation and a potential market correction on the horizon, the business model of Wall Street's elite may be tested.

Some are already adapting. They are finding unique service models to meet client demands and stay profitable, or relying on what many describe as a “generalist” approach that makes it easier to pivot away from, say, waning financial crisis litigation. And for many, the allure of the private equity market—once practically an afterthought—is becoming irresistible as that sector grows and early entrants like Latham & Watkins and Kirkland & Ellis reap the benefits.

Chart created by Jae Um of Six Parsecs and powered by data from ALM Intelligence's Legal Compass.

Chart created by Jae Um of Six Parsecs and powered by data from ALM Intelligence's Legal Compass.

Boom and Bust

“The financial crisis generated unprecedented amounts of big-ticket, franchise-threatening litigation and regulatory/enforcement work for leading Wall Street firms,” Paul, Weiss, Rifkind, Wharton & Garrison chairman Brad Karp says. More than 5,000 financial crisis litigations were filed, more than 1,000 enforcement and regulatory actions were brought against financial services firms, and law firms were paid tens of billions of dollars to prosecute and to defend these actions, Karp says.

Litigation departments at many of those firms swelled, along with in-house legal teams, to handle the huge demand.

But former banking executives say the peak came and went several years ago. “I can't imagine there was any big firm where their litigation budget didn't double” between the pre-crisis years and 2014, says a top banking source. Another says law firms fielded more work than at any other point in the last 30 years. The bulk of that litigation work went to Wall Street law firms and a few national firms, some former banking executives said.

Now, says Steven Gartner, co-chairman of Willkie Farr & Gallagher, “it's really a trickle, if it really exists at all.”

For the most part, firms haven't figured out what to replace it with. Banking clients are doling out less premium litigation work and the government isn't stimulating litigation through aggressive enforcement either.

“There has been a dramatic reduction in federal enforcement and regulatory activity, particularly targeted at financial services firms, under the Trump administration,” Karp says. “While some of the slack has been picked up by state regulators, there has been a material reduction in such activity.”

A former banking executive said the SEC appears to now be focused on low-level Ponzi schemes and cryptocurrency issues. “That's not the bread and butter for big Wall Street firms. They want to be representing JPMorgan Chase, Citi and Goldman,” he says.

So firms are looking for new opportunities.

At Cravath, Swaine & Moore, the three core practices remain litigation, M&A and financing. But the firm has been expanding its offerings around the edges. In the last two-and-a-half years, corporate department leader Mark Greene says, Cravath has launched a financial restructuring and reorganization practice, which he describes as more limited than bankruptcy work.

Greene says the firm was doing bank deals for the likes of Credit Suisse, JPMorgan and Citi, but if those deals went into restructuring, other firms got the work. Adding that capability has brought some notable matters to the firm, Greene says, including its representation of The Weinstein Co. and work related to Puerto Rico's economic crisis.

Greene says it speaks to the firm's focus on its lawyers being “ambidextrous,” and able to flow with shifts in the market.

Other firms point to a shift in the mix of litigation they are handling. At Paul Weiss, the litigation and regulatory practice has evolved since the end of the financial crisis to include more work generated by public companies and private equity firms, Karp says.

Sullivan & Cromwell replaced a lot of its litigation work for the financial services industry with work for Volkswagen and BP on mass torts-related matters.

Fried, Frank, Harris, Shriver & Jacobson chairman David Greenwald, who returned to the firm in 2013 after 20 years at Goldman Sachs, splits his firm's practice makeup into three buckets: private equity and M&A work; real estate, tax, finance, asset management and capital markets; and litigation and regulatory. The first two are going strong, backed by both private equity and investment bank clients, he says. But Greenwald would like to see more growth in the litigation group.

Like other firms, Fried Frank has seen the proportion of its revenue from litigation decline. But he sees opportunities in what he calls the firm's “strike zone,” such as financial-related matters, intellectual property and international arbitration.

“We are not expanding into areas that are outside of what our core competencies are,” Greenwald says.

'Draconian' Fee Pressure

As financial services litigation went into overdrive during the crisis, Wall Street banks also intensified fee pressure on their law firms, forcing double-digit discounts, alternative fee arrangements or the sharing of work with other providers. When the litigation died down, the expectations for discounted fees remained. In some cases, the pressure has been enough that firms opted to turn away bank work.

And it has tested a core assumption of Wall Street firms—that a high ratio of associates to partners fuels outsized profits.

Banks are putting pressure on firms to reduce leverage on their matters, one former bank executive says. “The business people are all about what you can do to keep costs down,” he notes. “A lot of legal work is commoditized. You don't need to have Cravath and Sullivan & Cromwell do confidentiality agreements.”

As consultant Jordan Furlong suggests, the recognition that there are alternatives for handling such work—including alternative legal providers—is spreading. A high-leverage model starts to break down if associates can't fill their time.

“They all sell a lot of overstaffed hours and I think that's what is really coming home to roost,” Furlong says.

Matthew Biben, co-leader of Debevoise & Plimpton's banking industry group, who joined the firm from JPMorgan in 2015, says banks are negotiating their own rates and pricing directly with discovery vendors and other alternative providers. “A sophisticated client is saying to you, 'We have retained a third-party service provider, a vendor to do first-level review of documents.' … It's relatively unsophisticated work and law firms before the financial crisis did that work themselves; it was fodder for first- and second-years,” Biben says.

For the work the firms are still doing, meanwhile, discount demands from clients have been steep. A banking industry source says by 2010, banks sometimes sought up to 30 percent off a multimillion-dollar engagement.

“[Banks] are one of the most demanding clients for Wall Street firms when it comes to discounting,” Willkie's Gartner says.

One law firm leader says “some banks have gone too far” in pushing for discounts, taking risks with their legal advice and relationships with firms.

CEOs, boards and others were imposing “draconian measures” to keep costs down in the wake of the financial crisis, says another law firm leader. “The volume of work was so great and leverage of work so great that law firms were basically willing to make the deal,” said the firm leader, who spoke anonymously to candidly describe the tensions.

As the work slowed, it got harder for law firms to justify intense discounts. There are clients “we just won't do work” for because of the discounting, the law firm leader says.

That's not to say firms are turning up their noses. “We still have long-standing relationships with all of our bank clients,” Shearman & Sterling senior partner David Beveridge says. “We're still on the panel of every financial institution, but we have to partner with financial institution clients to have effective fee arrangements.”

Aside from lower fees, banks are starting to look for different skill sets in their outside counsel, some firm leaders say. That has opened up opportunities for firms like Cooley, whose CEO, Joe Conroy, says he sees the institutional relationship between Wall Street banks and Wall Street firms breaking down to a degree.

“Not only are [banks] becoming less dominant in being able to drive high-margin work … but also, the new generations of bankers and private equity deal folks aren't saying, 'We have to go use XYZ Wall Street law firm on our deals,'” Conroy says.

Instead, he says, banks want firms that have ties to certain industries and can bring them deals in those sectors.

“These Wall Street firms, now many of them are waking up to the notion that they are going to need a company-side practice,” Conroy says, noting he has seen Wall Street firms become “way more aggressive” on pricing discounts and chasing work they wouldn't have touched before the recession.

Wall Street's New Look?

As the business calculus of their practices has changed and competitors have encroached, some Wall Street law firms have created new pricing models to adapt.

Randall Guynn and Margaret Tahyar, partners in Davis Polk & Wardwell's financial institutions group, say the practice, which provides regulatory advice to banking organizations, has increasingly offered services on fixed fees and shared-service models, where a group of banks are facing the same regulatory hurdle.

Davis Polk started its shared-service model around 2010. The firm creates a template with the common facts, and the client group shares the cost for the base template. Then each bank customizes it for its own situation. The firm has used the model to help deliver advice on the Volcker Rule, derivatives and living wills, Tahyar says.

Also around 2010, Davis Polk's financial institutions practice began hiring small groups of staff lawyers, whom the firm calls “specialized attorneys,” for low-cost financial regulatory services related to Dodd Frank. The attorneys, who are trained by Davis Polk, are billed at a lower cost than the firm's partnership-track associates.

That shift signals that Wall Street law firms are willing—or feel compelled—to compete with a growing brood of alternative legal services providers in the financial services industry. The question is how far up the legal services food chain those ASPs can get.

“If you are talking about the type of work that Wachtell [Lipton, Rosen & Katz] does, or Cravath—the highest levels of banking financial service counseling … that work is—and I suspect will for the foreseeable future continue to be—done principally by law firms,” consultant Mark A. Cohen of Legal Mosaic says.

But the work in the “fat middle” continues to spread to more competitors, he says.

Still, Davis Polk's financial institutions business has more than doubled in the last decade, Guynn says. Davis Polk and other firms point to new areas in which they are advising banks, such as in blockchain, fintech, cybersecurity and privacy.

Unlike other Wall Street firms, Cleary Gottlieb Steen & Hamilton never tied on to one bank as its main institutional client, says managing partner Michael Gerstenzang. Instead, it represented multiple banks in broader regulatory matters that fell outside other firms' expertise or ambitions.

“That kind of work really brings you to the inner sanctum of the banks, because lots of people can do deals, and the banks … are kind of deal machines, but every once in a while they have these regulatory issues that are bet-the-bank issues,” he says.

The financial crisis and related waterfall of regulatory issues strengthened Cleary's relationship with banking clients, Gerstenzang says. There is no question such activity is dying down, he acknowledges—but he says the firm is taking advantage of its international footprint to seize work overseas.

“The investigative techniques and the investigative aggressiveness that [the banks] witnessed in the U.S. now is being emulated outside the U.S.,” Gerstenzang says. “That happened five years ago in the U.K. or other places in Europe, but now it is broadening out.”

Knocking at Private Equity's Door

Perhaps the largest phenomenon to impact Wall Street firms is the rise in volume and prestige of private equity work—an area many Wall Street firms avoided until more recently.

“The investment banks used to be sought-after, prized clients for the Wall Street firms. Some of them still are,” says Kent Zimmermann, a consultant with the Zeughauser Group. “The change is that the private equity fund relationships are now just as prized in many cases—and in some cases, bigger prizes—and part of the reason why is because of the deal flow they generate relative to the investment banks.”

According to data from PitchBook, total private equity deal value and deal count have generally been on the rise each year since 2009, and the number of deals closed each year since 2014 has surpassed the pre-crisis high in 2007.

Dylan Cox, a PitchBook analyst, says the top private equity firms are more active, managing more capital, and there's been an increase in deals above the midmarket, such as those often done by KKR, Apollo and Blackstone. “Strong fundraising in recent years, coupled with favorable economic factors, has contributed to PE's strong investment momentum,” he says.

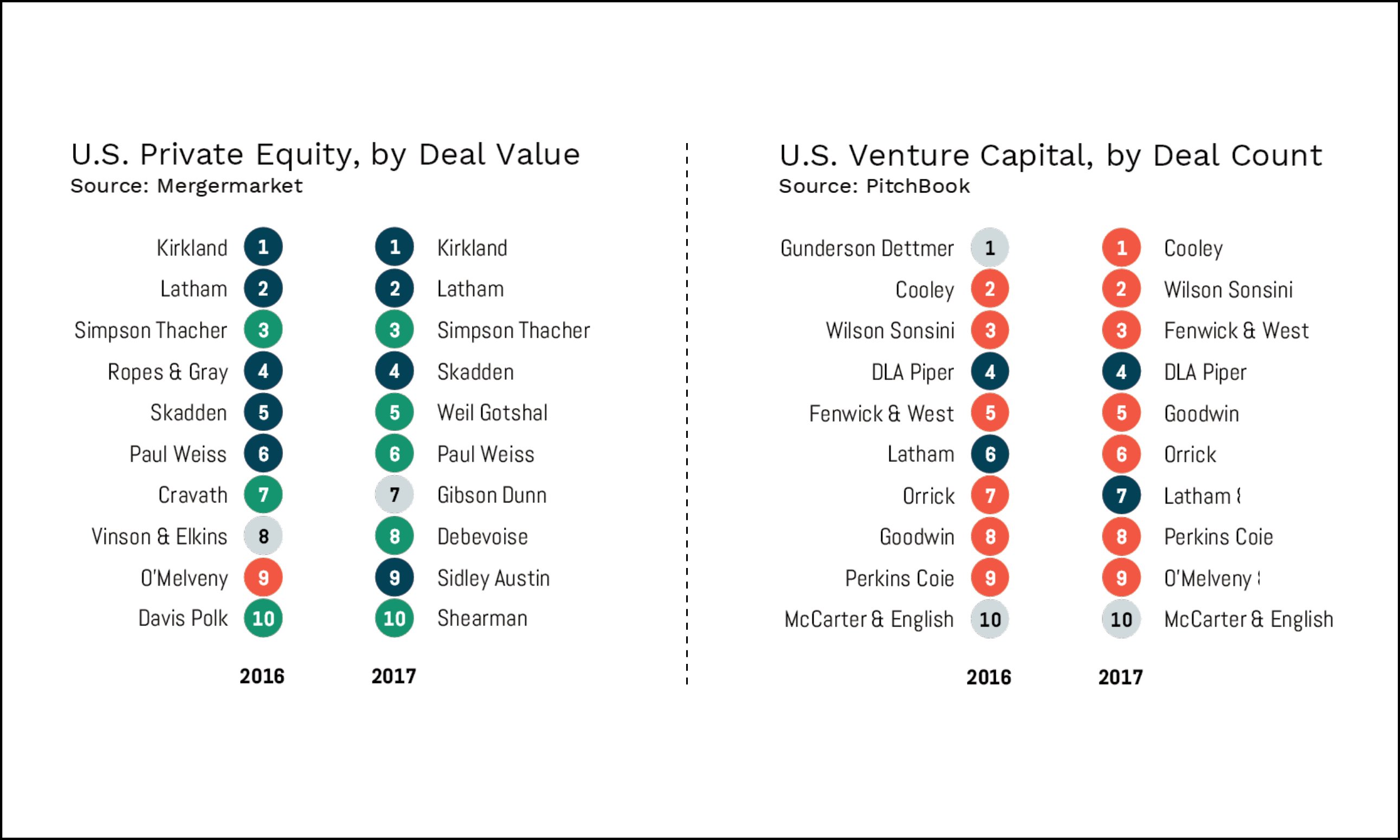

But despite the growing business opportunities, few Wall Street firms now regularly compete for the high-end work of representing the top private equity shops in their largest deals. According to Mergermarket's advisory league tables for 2017, the top two firms advising on U.S. private equity deal activity, by total deal value, were Kirkland & Ellis and Latham & Watkins. Simpson Thacher & Bartlett; Skadden, Arps, Slate, Meagher & Flom; Weil, Gotshal & Manges; and Paul Weiss rounded out the top six.

Chart created by Jae Um of Six Parsecs and powered by data from ALM Intelligence's Legal Compass.

Chart created by Jae Um of Six Parsecs and powered by data from ALM Intelligence's Legal Compass.

The Wall Street firms that are getting much of the work made key moves, such as Simpson Thacher establishing early relationships with KKR and Blackstone Group. Simpson Thacher did not comment for this article.

In 2011, Paul Weiss picked up a group of private equity partners from O'Melveny & Myers, helping the firm increase its market share in deals. Paul Weiss, which had represented Apollo in litigation, according to court records, began handling more deal work for Apollo after the lateral moves.

At Willkie, a “substantial majority” of the firm's revenue growth in the last five years is due to more work from private equity clients, including in deal work, fund formation and regulatory advice, Gartner says. While the dollar value of bank business fluctuates depending on particular litigation, the rise in private equity work means bank business is a smaller percentage of the firm's overall revenue than it was 10 years ago.

“A lot of the private equity work is midmarket,” according to Gartner, but those deals “can be very profitable.”

As a result of private equity becoming a growth area for the firm, Willkie has increased its partner head count in New York, London and Houston, where Willkie opened in late 2014. The firm now has about 30 lawyers in Houston, a predominantly private equity-based practice, Gartner says.

John Amorosi, an M&A partner at Davis Polk, says it has become “a strategic priority” to grow the firm's private equity business, with many of its existing M&A partners adding new clients and growing marketshare in the practice.

At Debevoise & Plimpton, private equity has been “a cornerstone” of the firm for about 30 years, says Kevin Schmidt, co-head of that practice area. While Schmidt says he has seen growing competition, he has also seen growing revenue in the business in recent years. He says the firm has invested in private equity by expanding related practices, including by adding laterals in enforcement and regulatory and in industries in which private equity invests, such as health care.

Private equity is no longer exclusively focused on leveraged buyouts. “The types of transactions that we are working on with private equity firms are broader,” Schmidt says.

Cadwalader Wickersham & Taft managing partner Patrick Quinn says the fastest-growing segment of the firm's business is from hedge funds and private equity funds, in part because those funds have entered businesses that were mostly dominated by banks.

One of Shearman's “target” industries is private capital, such as sovereign wealth funds, hedge funds and private equity funds, Beveridge says. “Private capital is a very good source of legal work,” he says, pointing to a consistent volume of work across M&A, litigation and restructuring, and finance.

Shearman most recently opened an office in Austin with partners who have practices in startups and private equity. “Midmarket private equity,” Beveridge says, is “a nice niche for us, and we've made some strides there and we'll continue to do that.”

At Milbank, Tweed, Hadley & McCloy, “more and more work” is coming from asset managers, private equity firms, hedge funds and mutual funds, says chairman Scott Edelman. They “have become very important players in the financial markets and that's made them important clients for law firms,” he says.

“They control more and more money,” Edelman says. “With regulation, banks are not able to do as much as they used to be able to pre-crisis, and more and more money is held and more and more transactions are being done by asset managers.”

Still, Edelman says, the firm's relationships with banks “remain very important to us.”

Indeed, several Wall Street law firms made clear that although they have growing business elsewhere, their bank representation is key. “Nobody is saying, 'We don't want to represent Goldman Sachs,'” Gartner says.

Meanwhile, firms that made bets on private equity decades ago are reaping big rewards. “A big part of Kirkland's rise has been driven by the fact that they've been pre-eminent in private equity, and the market has come to them,” Zimmermann says.

“Kirkland was ahead of everybody else,” acknowledged one law firm leader, adding, “The rise of private equity has added to the market pressures because the firms that have success there have enormous market clout.”

Kirkland declined to comment for this story.

Chart created by Jae Um of Six Parsecs and powered by data from ALM Intelligence's Legal Compass.

Chart created by Jae Um of Six Parsecs and powered by data from ALM Intelligence's Legal Compass.

Late to the Party?

While Wall Street firms say they are looking more closely at private equity, others privately question whether the firms are serious competition or could overcome the significant barriers to entry that exist in the current market.

Work performed for Latham's private equity clients has been the fastest-growing segment of its business in recent years, growing about twice as fast as overall firm growth, Latham's representatives say. “The ability to say we've represented KKR from the beginning, we represent Carlyle,” said Latham's Marc Jaffe, “opens a lot of doors.”

Jaffe, global co-chair for Latham's corporate department, and James Gorton, a Latham partner and member of the firm's executive committee, attribute Latham's success in private equity to the firm's early connections in the industry as well as Latham's deep talent pool in areas such as financing, tax, executive compensation and benefits, and the firm's industry expertise in areas such as energy and health care. “One or two people doesn't do the trick. You need to be able to do this with seriously deep benches with the highest-quality lawyers across the U.S. and across the globe,” Jaffe says about representing private equity firms in their complicated deals.

“You do see more [traditional] Wall Street firms,” Gorton says, “feel that they were late to the private equity party.” But the barriers to entry are high, he says.

“It's a growing, lucrative area, and they're trying to find ways to break in, but it takes more than just going and laterally hiring a deal professional. You really have to have an ecosystem around doing that kind of private equity work that takes enormous experience and investment,” Gorton says.

Amorosi, at Davis Polk, doesn't think it's too difficult for Wall Street law firms to compete with those that entered private equity decades ago. “At the end of the day, there's always a marketplace for good advice and talented and clever people,” he says.

Still, some Wall Street law firm leaders acknowledge the hurdles of building a private equity practice. It's difficult and expensive to bring on laterals who have experience and key client relationships, one says. Other lawyers say it takes a different type of lawyer and personality to deal with the business-minded clients on the private equity side.

One Am Law 50 leader says the desperation to get into private equity is causing some firms to make “outsized” hires, not only overpaying, but putting their firms' cultures at risk.

Another law firm leader says it can be challenging to represent the top private equity firms without adversely affecting bank clients. Conflicts can be managed by having different teams and offices and occupying different segments of the market, but navigating those conflicts is difficult, he says.

Cravath, whose leaders say it has punched above its weight on M&A deals despite fewer partners dedicated to that work than its peers, admits it has been historically “underweight” in the private equity arena and is looking to change that.

“Back before the global financial crisis, there were really four or five banks that absolutely dominated U.S. acquisition financing,” says Cravath's Richard Hall, a leading M&A partner at Cravath. “They are still significant players, but the collective market position is significantly smaller in percentage than it was in 2006-2007.”

That change is largely regulatory-driven, Hall notes, and it has opened up the opportunity for other financing sources to make inroads and thus created the need for firms like Cravath to make inroads with those financing sources.

“Over the last four to five years … private equity activity has become much more stable as a component of U.S. M&A activity,” Hall says. “That makes it a more attractive area for us because we think it plays to the basic strength of our M&A practice.”

Despite the opportunity, Cravath is still challenged to demonstrate its value when private equity firms are doing so many deals, Hall says. And by value, he partly means cost. Will a private equity firm want to pay Cravath's rates for such high volumes of work?

“But as private equity becomes more stable, we think we should get private equity activity back up to regular weighting,” he says.

Several market observers noted the rising financial clout of top private equity law firms as helping them peel away top talent from Wall Street lock-step firms. Look no further than Kirkland poaching two Cravath M&A partners in the last two years, including Eric Schiele and Jonathan Davis.

“Those unwanted departures are evidence of chinks in the armor” of some Wall Street firms, Zimmermann says.

Amorosi, at Davis Polk, cautions judging the success of certain lateral moves away from Wall Street firms. “I think the jury is out on that market development,” he says.

Shrink to Strength?

The strategic question in the long run, Gartner says, is whether higher leverage is sustainable. “Clients want efficiency and a higher level of attention,” he says.

Karp says firms face “a fundamental question” on whether changes from the financial crisis are temporary. It will determine how they approach staffing levels and resources in the future.

“What you've seen is a big change in the market. Firms that we've never heard of before, Latham, K&E, Jones Day,” one law firm leader notes, “they're all competing for the same work. Our competitors have grown from four or five to 40 firms, depending on the matter.”

Bruce MacEwen, a consultant with Adam Smith Esq., likens the changes among Wall Street firms to the changes the Magic Circle firms experienced over the last decade. Neither group is the homogeneous unit it once was, with the firms in each sector going in varying directions. That isn't necessarily a bad thing, he says. But like others, he wonders if shrinking is actually the best approach for Wall Street, even as some Wall Street firms tout their expanding international presence as a benefit.

“It doesn't seem to hurt Wachtell. Cravath has never been huge,” MacEwen says. “I would be tempted to say that's preferable; shrinking and maintaining impeccable quality is preferable to diluting things.”

Chart created by Jae Um of Six Parsecs and powered by data from ALM Intelligence's Legal Compass.

Chart created by Jae Um of Six Parsecs and powered by data from ALM Intelligence's Legal Compass.

Ten years and two presidents since his early-morning phone call, Cahill's Clark says things are back to normal. The financial industry learned its lessons from the Great Recession and deals are coming fast and furious. But the overall picture for Wall Street firms may not be as rosy.

How Wall Street firms replace the litigation drop-off, deal with new competition and handle a dip in deal flow when a recession hits will be the test of what “normal” means for the industry's elite. One thing is clear: These are tests Wall Street law firms never had to sit for before. They are faced with a concept foreign to them: competition.

Email: [email protected] and [email protected]. Charts created by Jae Um, founder of Six Parsecs and author of the companion piece to this article.

This content has been archived. It is available through our partners, LexisNexis® and Bloomberg Law.

To view this content, please continue to their sites.

Not a Lexis Subscriber?

Subscribe Now

Not a Bloomberg Law Subscriber?

Subscribe Now

NOT FOR REPRINT

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

You Might Like

View All

Covington, Steptoe Form New Groups Amid Demand in Regulatory, Enforcement Space

4 minute read

Consumer Finance Law Enforcer Takes Private Practice Job at Morgan Lewis

With 'Fractional' C-Suite Advisers, Midsize Firms Balance Expertise With Expense

4 minute readTrending Stories

Who Got The Work

J. Brugh Lower of Gibbons has entered an appearance for industrial equipment supplier Devco Corporation in a pending trademark infringement lawsuit. The suit, accusing the defendant of selling knock-off Graco products, was filed Dec. 18 in New Jersey District Court by Rivkin Radler on behalf of Graco Inc. and Graco Minnesota. The case, assigned to U.S. District Judge Zahid N. Quraishi, is 3:24-cv-11294, Graco Inc. et al v. Devco Corporation.

Who Got The Work

Rebecca Maller-Stein and Kent A. Yalowitz of Arnold & Porter Kaye Scholer have entered their appearances for Hanaco Venture Capital and its executives, Lior Prosor and David Frankel, in a pending securities lawsuit. The action, filed on Dec. 24 in New York Southern District Court by Zell, Aron & Co. on behalf of Goldeneye Advisors, accuses the defendants of negligently and fraudulently managing the plaintiff's $1 million investment. The case, assigned to U.S. District Judge Vernon S. Broderick, is 1:24-cv-09918, Goldeneye Advisors, LLC v. Hanaco Venture Capital, Ltd. et al.

Who Got The Work

Attorneys from A&O Shearman has stepped in as defense counsel for Toronto-Dominion Bank and other defendants in a pending securities class action. The suit, filed Dec. 11 in New York Southern District Court by Bleichmar Fonti & Auld, accuses the defendants of concealing the bank's 'pervasive' deficiencies in regards to its compliance with the Bank Secrecy Act and the quality of its anti-money laundering controls. The case, assigned to U.S. District Judge Arun Subramanian, is 1:24-cv-09445, Gonzalez v. The Toronto-Dominion Bank et al.

Who Got The Work

Crown Castle International, a Pennsylvania company providing shared communications infrastructure, has turned to Luke D. Wolf of Gordon Rees Scully Mansukhani to fend off a pending breach-of-contract lawsuit. The court action, filed Nov. 25 in Michigan Eastern District Court by Hooper Hathaway PC on behalf of The Town Residences LLC, accuses Crown Castle of failing to transfer approximately $30,000 in utility payments from T-Mobile in breach of a roof-top lease and assignment agreement. The case, assigned to U.S. District Judge Susan K. Declercq, is 2:24-cv-13131, The Town Residences LLC v. T-Mobile US, Inc. et al.

Who Got The Work

Wilfred P. Coronato and Daniel M. Schwartz of McCarter & English have stepped in as defense counsel to Electrolux Home Products Inc. in a pending product liability lawsuit. The court action, filed Nov. 26 in New York Eastern District Court by Poulos Lopiccolo PC and Nagel Rice LLP on behalf of David Stern, alleges that the defendant's refrigerators’ drawers and shelving repeatedly break and fall apart within months after purchase. The case, assigned to U.S. District Judge Joan M. Azrack, is 2:24-cv-08204, Stern v. Electrolux Home Products, Inc.

Featured Firms

Law Offices of Gary Martin Hays & Associates, P.C.

(470) 294-1674

Law Offices of Mark E. Salomone

(857) 444-6468

Smith & Hassler

(713) 739-1250