How the rise of the US elite in London has shaken up the M&A market

Post-crisis M&A trend data highlights battle for dominance at top end of market

February 28, 2017 at 04:12 AM

5 minute read

Much has been written about the growing influence of US law firms in the UK legal market. US firms have been developing their English law capability for the past 20 years or so, but the major M&A firms have made a particular push since the 2008 recession. We can now see the results of these efforts.

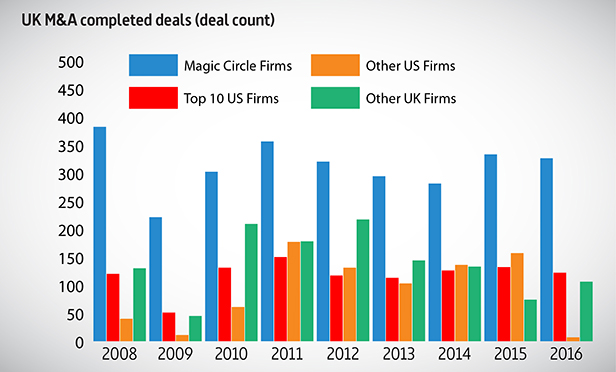

We have reviewed the Thomson Reuters M&A data of completed transactions for the nine years to the end of 2016. We then segmented the market by reference to the five magic circle firms, the 10 US firms having the highest aggregate completed deal value in the entire period, other UK firms and other US firms.

What is now clear is that the top 10 US law firms have significantly grown their market share during the period, although it is unclear if they will sustain the position they achieved in 2014 and 2016. The other US firms have generally been less successful and the other UK firms have generally flatlined (but with a good 2016).

In effect, not only in the UK but across Europe and globally, a relatively small group of UK firms (the magic circle) and US firms (primarily New York-based) are increasingly dominating the big-ticket M&A work with a value of more than $5bn.

Although this may be a relatively small percentage of the overall number of transactions, these deals tend to be the most complex, international and highly remunerated of all M&A work. It appears that, in effect, a global club of law firms has emerged that are trusted by the investment banks and the major corporates to undertake their biggest transactions.

The data inevitably comes with a number of health warnings. Some of the data may be incomplete – especially in relation to smaller transactions; some firms may have been credited with a role in a transaction when in reality they were not the key advisers; large multi-country transactions are likely to have major UK and US advisers acting for the parties so some of the UK deals credited to US firms may not have related to English law advice (for example, Wachtell Lipton Rosen & Katz, which does not have a London office, makes the top 10 list in value terms); and one or two 'blockbuster' deals can have a disproportionate effect upon a firm's position in any one year, especially if M&A activity is otherwise subdued. By definition, the magic circle is five firms, whereas the top 10 US firms represents 10 firms, so level pegging in the tables would mean that on average each magic circle firm is doing double the value of each of the top 10 US firms.

When looking at the number of transactions, the message is more mixed. The magic circle clearly dominates in the number of transactions, with the other three categories at broadly level pegging (with the other US firms having a good 2015 but a poor 2016).

Although some US firms have a large UK presence, many of the most successful in M&A terms have been very focused. They have hired top partners, often from magic circle firms, and work very closely with their New York and European colleagues. Generally, they are very clear as to the work they do and don't do, and have not been tempted to engage in mission creep.

For other US and UK firms, it may not be credible for them to consistently capture the mega-transactions, and in a very competitive market they need clarity as to the type of transactions, the type of clients or the industry sectors in which their strength lies.

It is increasingly clear from the other Thomson Reuters tables that across Europe and globally, a strong group of US law firms are increasingly potent competition to the magic circle. They tend to have a much smaller international platform than most of the magic circle firms and are generally significantly more profitable.

The fact that some have gained sufficient capability and credibility in London to advise on both the US and English law aspects of a transaction is in contrast to most of the magic circle firms, which have spent many years and many millions in New York but without, as yet, consistently achieving the same breakthrough.

The US firms' focused approach means that they do not wish to hire swathes of magic circle partners, but they have a strong armoury when they do go looking. If they are able to sustain the momentum they have developed, it may cause some magic circle firms to question their model and the size and breadth of their international operations.

If, as appears to be the case, a club of US and UK firms has emerged to undertake the largest and most complex global transactions, then we are likely to see battles for dominance within that club and the need for firms outside to be more realistic about their market position.

Tony Williams is the founder of Jomati Consultants and the former managing partner of Clifford Chance.

This content has been archived. It is available through our partners, LexisNexis® and Bloomberg Law.

To view this content, please continue to their sites.

Not a Lexis Subscriber?

Subscribe Now

Not a Bloomberg Law Subscriber?

Subscribe Now

NOT FOR REPRINT

© 2024 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

You Might Like

View All

A&O Shearman, Hogan Lovells & 10 Top Stories That Shaped Africa in 2024

4 minute read

Borden Ladner Gervais Cyber Expert Warns of Growing Threats From AI-Boosted Ransomware Attacks

3 minute read

Baker & Partners, LCWP Lead on $1B Fraud Claim by Malaysia's 1MDB Against Amicorp

Trending Stories

- 1'Largest Retail Data Breach in History'? Hot Topic and Affiliated Brands Sued for Alleged Failure to Prevent Data Breach Linked to Snowflake Software

- 2Former President of New York State Bar, and the New York Bar Foundation, Dies As He Entered 70th Year as Attorney

- 3Legal Advocates in Uproar Upon Release of Footage Showing CO's Beat Black Inmate Before His Death

- 4Longtime Baker & Hostetler Partner, Former White House Counsel David Rivkin Dies at 68

- 5Court System Seeks Public Comment on E-Filing for Annual Report

Who Got The Work

Michael G. Bongiorno, Andrew Scott Dulberg and Elizabeth E. Driscoll from Wilmer Cutler Pickering Hale and Dorr have stepped in to represent Symbotic Inc., an A.I.-enabled technology platform that focuses on increasing supply chain efficiency, and other defendants in a pending shareholder derivative lawsuit. The case, filed Oct. 2 in Massachusetts District Court by the Brown Law Firm on behalf of Stephen Austen, accuses certain officers and directors of misleading investors in regard to Symbotic's potential for margin growth by failing to disclose that the company was not equipped to timely deploy its systems or manage expenses through project delays. The case, assigned to U.S. District Judge Nathaniel M. Gorton, is 1:24-cv-12522, Austen v. Cohen et al.

Who Got The Work

Edmund Polubinski and Marie Killmond of Davis Polk & Wardwell have entered appearances for data platform software development company MongoDB and other defendants in a pending shareholder derivative lawsuit. The action, filed Oct. 7 in New York Southern District Court by the Brown Law Firm, accuses the company's directors and/or officers of falsely expressing confidence in the company’s restructuring of its sales incentive plan and downplaying the severity of decreases in its upfront commitments. The case is 1:24-cv-07594, Roy v. Ittycheria et al.

Who Got The Work

Amy O. Bruchs and Kurt F. Ellison of Michael Best & Friedrich have entered appearances for Epic Systems Corp. in a pending employment discrimination lawsuit. The suit was filed Sept. 7 in Wisconsin Western District Court by Levine Eisberner LLC and Siri & Glimstad on behalf of a project manager who claims that he was wrongfully terminated after applying for a religious exemption to the defendant's COVID-19 vaccine mandate. The case, assigned to U.S. Magistrate Judge Anita Marie Boor, is 3:24-cv-00630, Secker, Nathan v. Epic Systems Corporation.

Who Got The Work

David X. Sullivan, Thomas J. Finn and Gregory A. Hall from McCarter & English have entered appearances for Sunrun Installation Services in a pending civil rights lawsuit. The complaint was filed Sept. 4 in Connecticut District Court by attorney Robert M. Berke on behalf of former employee George Edward Steins, who was arrested and charged with employing an unregistered home improvement salesperson. The complaint alleges that had Sunrun informed the Connecticut Department of Consumer Protection that the plaintiff's employment had ended in 2017 and that he no longer held Sunrun's home improvement contractor license, he would not have been hit with charges, which were dismissed in May 2024. The case, assigned to U.S. District Judge Jeffrey A. Meyer, is 3:24-cv-01423, Steins v. Sunrun, Inc. et al.

Who Got The Work

Greenberg Traurig shareholder Joshua L. Raskin has entered an appearance for boohoo.com UK Ltd. in a pending patent infringement lawsuit. The suit, filed Sept. 3 in Texas Eastern District Court by Rozier Hardt McDonough on behalf of Alto Dynamics, asserts five patents related to an online shopping platform. The case, assigned to U.S. District Judge Rodney Gilstrap, is 2:24-cv-00719, Alto Dynamics, LLC v. boohoo.com UK Limited.

Featured Firms

Law Offices of Gary Martin Hays & Associates, P.C.

(470) 294-1674

Law Offices of Mark E. Salomone

(857) 444-6468

Smith & Hassler

(713) 739-1250