Is the top end of the legal market finally ready for transatlantic consolidation?

Following the Eversheds Sutherland tie-up and the Norton Rose-Chadbourne talks, Chris Johnson looks at the prospects for more major UK-US merger deals

February 10, 2017 at 06:35 AM

7 minute read

The consolidation of the legal market across the Atlantic has been talked up for decades.

Any time there's a major deal between US and UK firms, people start heralding the onset of transatlantic merger 'mania', which is about the least appropriate word I can think of to describe what is usually a protracted, painstaking process.

Each time, the anticipated wave of follow-on deals fails to materialise. So far, the transatlantic merger trend has been more of a squeak than a big bang. Could that be about to change?

The recent marriage of Eversheds and Atlanta-based Sutherland Asbill & Brennan, and the news that Norton Rose Fulbright is in talks with Chadbourne & Parke – a deal that would finally give the global giant the New York presence it has long craved – has brought the issue back into sharp focus.

In this post-Brexit, post-Donald Trump world of uncertainty, forecasting is a game for the foolish and foolhardy. But I'll give it a go. Looking purely at large-scale transatlantic combinations, rather than the acquisition of smaller practices, I'd bet on there being a handful of additional deals in the coming years. But don't expect a glut.

For any individual firm, there will only be a reasonably small number of transatlantic targets with the right mix of practice areas and sectors, broadly comparable financial performance – particularly around rates and profitability – and, perhaps most importantly of all, a compatible culture. Scrub out the firms that have no international aspirations or interest in merging, and the shortlist becomes shorter still. It's like searching for a needle in a haystack made entirely of other needles. (Also: without extreme care, you're liable to get hurt.)

Secondly, without wanting to state the blindingly obvious, law firm mergers are incredibly difficult to pull off. At every stage, from finding a suitable candidate to actually getting the deal approved by partnerships that are generally risk and change averse, they are fraught with complications.

This is doubly true of transatlantic mergers, where firms face the complex and potentially costly issue of reconciling contrasting tax, accounting and partner compensation arrangements. Most large UK firms operate accruals-based accounting systems with a year-end of 30 April, and compensate partners via some form of lockstep. US firms, meanwhile, typically utilise cash-based accounting setups with a calendar financial year. They also tend to reward partners based more on individual merit.

A Swiss verein – a holding structure that allows member firms to join forces yet retain their existing forms – sidesteps or at least mitigates many of these hurdles, but serious challenges remain. (Almost every recent major cross-border law firm combination has been carried out via a verein, including those that formed Dentons, DLA Piper, Hogan Lovells, King & Wood Mallesons, Norton Rose Fulbright and Squire Patton Boggs.)

It is unsurprising, then, that while merger talks between firms are actually pretty common – at any one time, it's likely that some form of discussion is ongoing somewhere in the market – the vast majority never materialise. Even among those that make it to an advanced stage, the failure rate is still relatively high. Last year, Greenberg Traurig pulled out of its proposed tie-up with Berwin Leighton Paisner amid concerns about the London-based firm's practice mix, culture and management. And a deal between Hunton & Williams and Addleshaw Goddard was put on hold in August due to concerns over the Brexit vote.

There does now seem to be more interest among firms in transatlantic deals than ever before, however. And the more that actually go ahead, the more other firms are likely to follow suit, so as not to be left behind by newly expansive rivals.

One magic circle management partner told me that his firm is 'open-minded' about the prospect of a US merger

Combinations could also be driven by firms wanting to move while choice targets still remain, although we're a long way from the situation in Germany in the late 1990s, when international firms flooded the market and had to fight over a rapidly diminishing number of local practices. During an 18-month period, those local practices were almost all acquired by US and UK interlopers.

Mid-sized firms are under particular pressure to act, with many lacking the scale or specialisation to adequately differentiate themselves in an increasingly competitive market. Look across the US top 200 and you'll see many firms with hundreds of lawyers who are largely doing the same sort of work for the same sort of clients. That is not a viable long-term strategy. Smaller practices with fewer – if any – international offices are also less equipped to deal with the continued globalisation of legal services.

But perhaps the most significant question is the extent to which the elite firms will get involved. There has only ever been one transatlantic deal involving a white shoe or magic circle law firm: the merger between Clifford Chance and New York's Rogers & Wells in 2000. And that didn't exactly go well.

A merger could be one way for the magic circle firms to resolve their longstanding struggle to build scale in the US, where despite decades of investment, they remain largely peripheral players. Likewise, for US firms in London, where interest in growth remains high despite the UK's decision to leave the EU. There are already about 90 US firms with offices in London, collectively employing more than 6,000 lawyers. But most have failed to reach a critical mass in the UK. Excluding the products of large-scale transatlantic mergers, such as DLA Piper and Hogan Lovells, just 10 US firms have more than 100 lawyers in London, according to NLJ 500 data. Most have fewer than 60.

Such top-tier deals have always been considered unlikely, mainly due to an assumption that the magic circle would only be interested in the top Wall Street firms, which are significantly more profitable than their UK rivals and seemingly not interested in merging anyway. That may have been the case in the past, but the magic circle firms seem to have broadened their approach.

One magic circle management partner told me that his firm is "open-minded" about the prospect of a US merger and said there is "a lot of quality" beyond the white-shoe firms. And while the magic circle may lack the financial firepower of the top New York practices, you don't have to go too far down the Am Law 100 charts before the profitability gap begins to close.

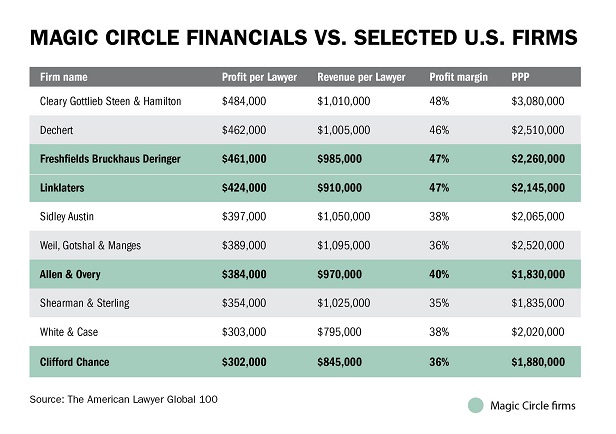

When viewed across a range of metrics, including profit margin, revenue and profit per lawyer (RPL and PPL), and profit per equity partner (PEP), they are in the same ballpark as firms such as Dechert, Sidley Austin, Shearman & Sterling and Weil Gotshal & Manges. And that's as measured in US dollars, even after an unfavourable currency conversion resulting from a historically weak British pound.

Freshfields Bruckhaus Deringer's margin, RPL and PPL are actually within a few percent of Cleary Gottlieb Steen & Hamilton – it is only distanced on PEP by virtue of having a larger equity partnership.

Despite the considerable strides being made in London by Latham & Watkins and White & Case, no single law firm has successfully established itself as a true market leader on both sides of the Atlantic. When viewed in that context, a transatlantic deal involving an elite American or British law firm could be a genuine game changer.

NOT FOR REPRINT

© 2025 ALM Global, LLC, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more information visit Asset & Logo Licensing.

You Might Like

View All

'Almost Impossible'?: Squire Challenge to Sanctions Spotlights Difficulty of Getting Off Administration's List

4 minute read

'Never Been More Dynamic': US Law Firm Leaders Reflect on 2024 and Expectations Next Year

7 minute readTrending Stories

- 1Data Breach Lawsuit Against Byte Federal Among 1,500 Targeting Companies in 2024

- 2Counterfeiters Ride Surge in Tabletop Games’ Popularity, Challenging IP Owners to Keep Up

- 3Health Care Data Breach Class Actions Saw December Surge in NY Courts

- 4Florida Supreme Court Disbars 3, Suspends 11, Reprimands 1 in Final Disciplinary Order of 2024

- 5Chief Justice Roberts Ends Year With Defense Against 'Illegitimate' Attacks on Judiciary

Who Got The Work

Michael G. Bongiorno, Andrew Scott Dulberg and Elizabeth E. Driscoll from Wilmer Cutler Pickering Hale and Dorr have stepped in to represent Symbotic Inc., an A.I.-enabled technology platform that focuses on increasing supply chain efficiency, and other defendants in a pending shareholder derivative lawsuit. The case, filed Oct. 2 in Massachusetts District Court by the Brown Law Firm on behalf of Stephen Austen, accuses certain officers and directors of misleading investors in regard to Symbotic's potential for margin growth by failing to disclose that the company was not equipped to timely deploy its systems or manage expenses through project delays. The case, assigned to U.S. District Judge Nathaniel M. Gorton, is 1:24-cv-12522, Austen v. Cohen et al.

Who Got The Work

Edmund Polubinski and Marie Killmond of Davis Polk & Wardwell have entered appearances for data platform software development company MongoDB and other defendants in a pending shareholder derivative lawsuit. The action, filed Oct. 7 in New York Southern District Court by the Brown Law Firm, accuses the company's directors and/or officers of falsely expressing confidence in the company’s restructuring of its sales incentive plan and downplaying the severity of decreases in its upfront commitments. The case is 1:24-cv-07594, Roy v. Ittycheria et al.

Who Got The Work

Amy O. Bruchs and Kurt F. Ellison of Michael Best & Friedrich have entered appearances for Epic Systems Corp. in a pending employment discrimination lawsuit. The suit was filed Sept. 7 in Wisconsin Western District Court by Levine Eisberner LLC and Siri & Glimstad on behalf of a project manager who claims that he was wrongfully terminated after applying for a religious exemption to the defendant's COVID-19 vaccine mandate. The case, assigned to U.S. Magistrate Judge Anita Marie Boor, is 3:24-cv-00630, Secker, Nathan v. Epic Systems Corporation.

Who Got The Work

David X. Sullivan, Thomas J. Finn and Gregory A. Hall from McCarter & English have entered appearances for Sunrun Installation Services in a pending civil rights lawsuit. The complaint was filed Sept. 4 in Connecticut District Court by attorney Robert M. Berke on behalf of former employee George Edward Steins, who was arrested and charged with employing an unregistered home improvement salesperson. The complaint alleges that had Sunrun informed the Connecticut Department of Consumer Protection that the plaintiff's employment had ended in 2017 and that he no longer held Sunrun's home improvement contractor license, he would not have been hit with charges, which were dismissed in May 2024. The case, assigned to U.S. District Judge Jeffrey A. Meyer, is 3:24-cv-01423, Steins v. Sunrun, Inc. et al.

Who Got The Work

Greenberg Traurig shareholder Joshua L. Raskin has entered an appearance for boohoo.com UK Ltd. in a pending patent infringement lawsuit. The suit, filed Sept. 3 in Texas Eastern District Court by Rozier Hardt McDonough on behalf of Alto Dynamics, asserts five patents related to an online shopping platform. The case, assigned to U.S. District Judge Rodney Gilstrap, is 2:24-cv-00719, Alto Dynamics, LLC v. boohoo.com UK Limited.

Featured Firms

Law Offices of Gary Martin Hays & Associates, P.C.

(470) 294-1674

Law Offices of Mark E. Salomone

(857) 444-6468

Smith & Hassler

(713) 739-1250